RETURNING TO THE GOLD STANDARD IN FIVE EASY STEPS

You hear a lot of people in the United States talking about returning to the Gold Standard today. With trillion-dollar annual government deficits, a declining dollar, and fears of inflation, many people feel a return to the Gold Standard would solve these problems by forcing the government to be more financially and fiscally conservative. Currently, the US issues a fiat currency which has no backing and whose value depends upon its credibility.

If the US has higher inflation than other countries, offers lower interest rates or fewer investment opportunities, demand for the US Dollar goes down and so does the value of the Dollar. If the opposite occurs, the value of the Dollar rises. Some people feel the Fed has done a poor job of maintaining the value of the US Dollar, and that a fiat currency gives the Federal Government too much freedom to spend money since they can print more dollars and issue more debt to cover any Federal Government deficits. Returning to the Gold Standard would be one way of controlling government spending and provide price stability since it would eliminate the “freedoms” provided by a fiat currency and impose fiscal responsibilities that are often ignored.

What is rarely heard in this debate is if the United States actually decided to return to the Gold Standard, how would it get there? What steps would have to be taken in order to return the United States to a fully functioning Gold Standard that existed throughout the World prior to World War I? This paper is designed to answer that question.

STEP 1: DECLARE THE VALUE OF THE US DOLLAR IN TERMS OF GOLD

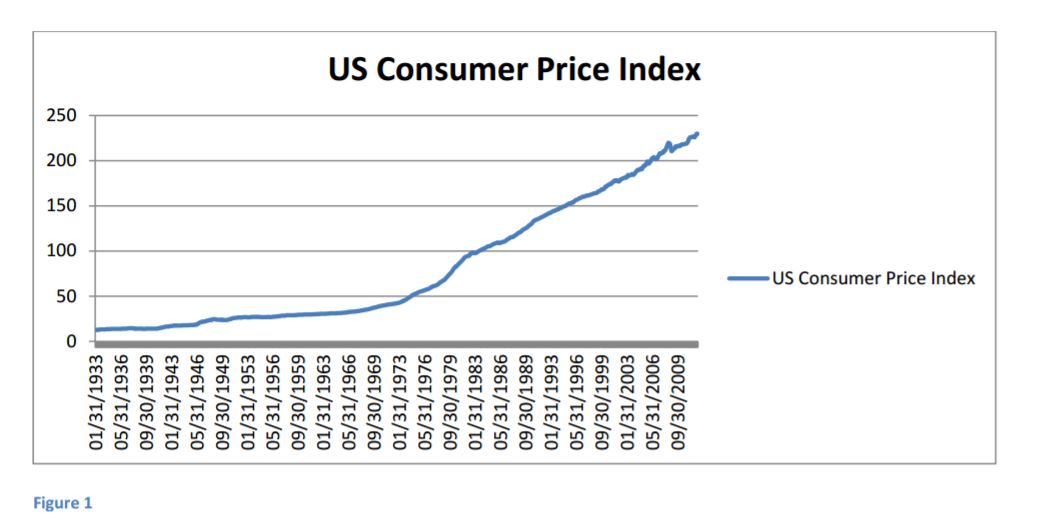

The United States issued gold coins during most years between 1795 and 1933 when the United States abandoned the Gold Standard and made it illegal (until 1974) for Americans to own gold. Under the Gold Standard, the value of the US Dollar was set at $20.67. A $20 gold piece contained almost 1 ounce of gold and existed as a medium of exchange.

Given the inflation that has occurred in the United States since 1933 (Figure 1), it would be unrealistic to return to the old price of gold at $20.67, especially since the price was raised to $35 under Roosevelt and $42.22 under Nixon before abandoning gold completely.

One simple solution would be to devalue Federal Reserve Notes and declare that 100 Federal Reserve Dollars are equal to 1 Gold Dollar. This would set the value of Gold in terms of the US Dollar at $2067. Since this rate is higher than the market price, the Government’s announcement would attract gold into the US Treasury so the United States could replenish its gold reserves. Of course, this action would lead to some inflation in the United States and possible depreciation of the US Dollar, but that would be one cost of moving to a Gold Standard.

Once the value of the US Dollar was redefined at $2067 an ounce, the United States would have to maintain that price. As long as the market price of gold was at $2067 or below, the United States Government would buy any gold it was offered. But what would happen if the market price exceeded $2067?

If the market price of gold were to exceed the predefined $2067, people would simply stop selling gold to the US Treasury at this price. In the old days, this would cause an outflow of gold to other countries which offered a higher relative price for gold, but until other countries joined the Gold Standard (The Euro might be set at 1500 Euros = 1 ounce of gold or 1250 British Pounds = 1 Ounce of gold, etc.), there would be no foreign government treasury the gold could flow to.

Instead, the gold would flow into private hands. The United States would have to take measures to push the market price of Gold back to $2067 to defend the Gold Dollar. The government could do this by either raising interest rates, increasing the return on Gold Dollars, or by introducing monetary policies that would cause deflation. In the short run, financial flows determine the value of currencies, so the focus would be on using monetary policy to maintain the fixed price of gold. This would lead to step 2.

STEP 2: CHANGE THE FEDERAL RESERVE’S MISSION TO MAINTAINING THE VALUE OF THE GOLD DOLLAR

Currently, the Federal Reserve has several goals it tries to achieve. The Federal Reserve is supposed to simultaneously control inflation, keep unemployment to acceptable levels, promote growth and employment in the economy, maintain the value of the US Dollar and promote a stable financial system. The problem is some of these goals run contrary to each other. Reducing unemployment may contribute to inflation, while controlling inflation may slow growth and increase unemployment. So the Fed has to determine which of these goals is the most important at any point in time, and focus on that goal at the expense of the others. If the economy is in a recession, the Fed decides to promote growth even if some inflation occurs. If inflation is spiraling out of control, the Fed fights inflation even though it may slow growth and lead to some unemployment.

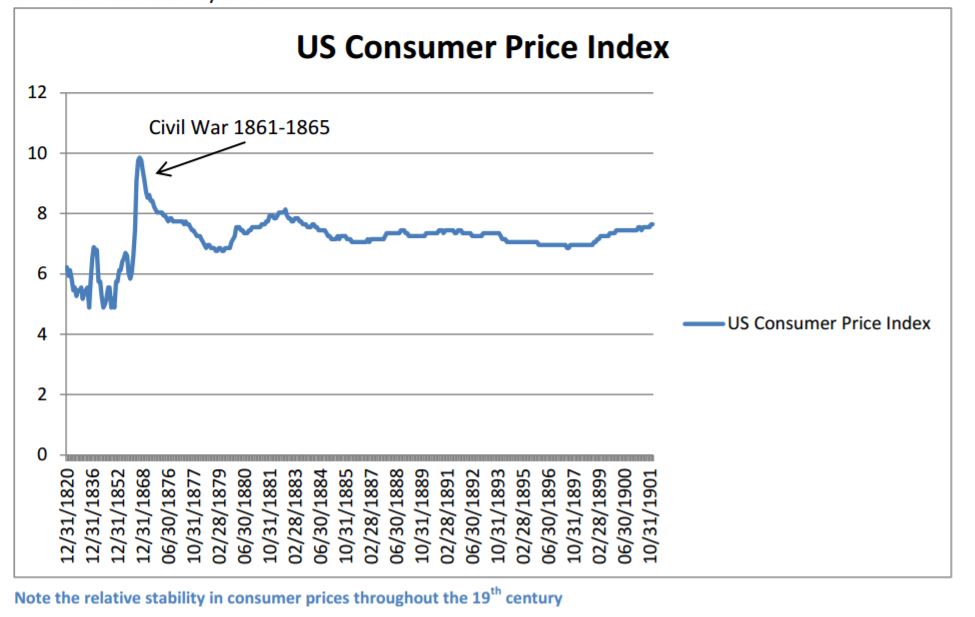

The benefit of returning to a Gold Standard is that it simplifies life for the Fed tremendously. No more worrying about unemployment and growth, just focus on maintaining the value of the US Dollar relative to gold. During the 1800s, there were long periods of deflation and slow growth that occurred and this could become a possibility during the 2000s. On the other hand, under a Gold Standard there would be little need to worry about double-digit or even single-digit inflation slowly destroying the value of assets and the US Dollar.

Returning to a Gold Standard would also mean an end to financial bubbles since there is no expansion of fiat currency to keep the bubble going. A gold standard means stable asset prices as well as stable prices for goods. As in the 1800s, stock market prices might change little from one decade to the next because stock prices would respond to real, not inflated profits. Homeowners wouldn’t have to worry about housing prices rising and making housing unaffordable (but existing homeowners couldn’t expect the value of their houses to rise every year either). A return to the Gold Standard would mean that money that would have been channeled into assets for speculation could be redirected to real assets.

Of course, if the Gold Standard worked so well in the 1800s, why did countries abandon it? Simple, almost every time a country left the Gold Standard it was caused by one thing: Government Deficits. During the 1800s, most governments were relatively small, so government deficits were almost always caused by war. Great Britain suspended the convertibility of paper pounds into gold during the Napoleonic Wars and the United States (Federal and Confederate) suspended the convertibility of paper dollars during the Civil War. However, in both cases, after these wars, the countries deflated, governments maintained budget surpluses, and they paid down existing debt to return to the Gold Standard.

What really killed the Gold Standard more than anything else was World War I. The levels of debt, the economic dislocations and the post-war costs associated with the Great War were so huge that returning to the old fixed rates of gold proved impossible. Britain’s attempts to return to the old definition of gold devastated the economy. Although there were numerous international conferences during the 1920s and 1930s to attempt to reinstitute the Gold Standard, these attempts all failed. With no international agreement, each country chose to use fiscal and monetary expansion over the Gold Standard.

But if the United States moved back to the Gold Standard, it would have to return to fiscal stability so there would be no threat of the United States being forced to suspend the convertibility of paper dollars into Gold Dollars. Hence, step 3.

STEP 3: PASS A BALANCED BUDGET AMENDMENT TO THE UNITED STATES CONSTITUTION

Of course, Congress would not only have to pass a Balanced Budget Amendment, but give it credibility so that other countries as well as America’s own citizens knew that balancing the budget was paramount over all other Fiscal goals. In an age when the United States Congress can’t even pass a budget and uses Continuing Resolutions as a way of keeping the government from grinding to a halt, this would be a huge step.

To give full credibility to this goal, the United States would need to add a Balanced Budget Amendment to the United States Constitution. This would require that the bill to be passed by two thirds of both houses of Congress and then ratified by three-fourths of the states. Some would argue that this would take a long-time, but that isn’t necessarily so. When the United States decided to end Prohibition, Congress proposed the 21st Amendment on February 20, 1933 and it was adopted through state ratifying conventions on December 5, 1933. And let’s be honest here, isn’t balancing the budget more important than getting drunk? It’s just a matter of setting priorities.

Of course, it isn’t necessary to pass a balanced budget every single year in order to maintain the new Gold Standard, or to pay off existing Federal government debt. Britain spent a century gradually paying down the costs of the Napoleonic wars. The key is that the government should provide credibility to maintaining the fixed price of one ounce of gold equals $2067 US Dollars. So what could go wrong?

- War. This is what usually pushed countries off of the Gold Standard. Countries were simply

unable to raise taxes enough to pay for a war, so they borrowed money and paid off the debt over time. This means that if the United States wants to fight abroad, people have to realize that wars mean higher taxes under a Gold Standard, not adding to the deficit.

- Social Security. When the Gold Standard existed in the 1800s, there was no Social Security.

One of the principal fears that people have concerning future budgets is the impact of rising social security costs on budget deficits. Adopting the Gold Standard does not mean abandoning Social Security, but to stay on the Gold Standard, the United States would have to provide credibility to limiting expenditures on Social Security. The easiest way would be to allocate a fixed amount of GDP to Social Security Expenditures each year and never

breech that amount. The retirement age could be raised, and/or means testing could be introduced to reduce future Social Security costs. Each year, Social Security benefits would have to adjust to fit within those limits. This might mean lowering Social Security benefits in some years if the economy shrank or was in a recession, or a form of the Negative Income Tax could be used as a kind of means testing. Either way, Social Security would have to take

second place to maintaining the Gold Standard.

- Medicare and Medicaid. Compared to the projected growth in the costs of Medicare as the

Baby Boomers age and medical technology advances and costs increase, Social Security is a minor concern. The only way to control medical expenditures is to provide less medical care. In order to maintain balanced budgets, the government would have to cap medical spending. This could be done in several ways. Co-pays could be introduced, payments could be tied to the health of the individual, and caps could be placed on total government

expenditures on each person. Some estimates have shown that Medicare recipients receive three times as much in benefits as they pay in. Obviously, this is unsustainable. Like any insurance program, expenditures and revenues must balance. Inevitably, this would mean denying some medical care and making a cost-benefit analysis of medical care a priority over trying to extend life no matter what the cost. If the government never says no, medical

costs will never stop rising.

- Other government transfers. The Federal Government transfers large amounts of money to

the states, municipalities, and foreign governments, and provides bailouts to banks and corporations such as General Motors. Under a Gold Standard, no private or public entity should be allowed to receive transfers from the Federal Government. If states issue bonds to spend money they don’t have and they can’t pay those bonds, they default. If businesses fail, they go bankrupt. If banks fail, they shut their doors. If governments default, creditors have to bear the costs. The Federal Government could, in some cases, act as a lender of last

resort when liquidity is a problem, but bailouts for insolvency that imperil the balanced budget would have to end.

- Countercyclical Fiscal Policy. Keynesian theory encourages the government to run deficits

during recessions and surpluses during expansions. The problem is that governments are good at running deficits during recessions, but poor at running surpluses during expansions to pay off the incurred debt. Any current deficit would have to be fully offset by future surpluses. Without a guarantee of a future surplus, the deficit could not be incurred. Hoping fiscal policy would balance itself of its own accord would have to be abandoned.Assuming that none of the consequences of restricting fiscal policy to maintain a balanced budget and adhere to the new Gold Standard are unacceptable, what would be the next step?

STEP 4. ELECT GOLD-STANDARD POLITICIANS.

Given the current (or maybe eternal is a better word) low standing of politicians, this might be the most difficult step of all. And if the government virtually collapses over raising the debt ceiling, what would happen if it debated introducing a new Gold Standard?

But if politicians want to redeem themselves, this could be one way of doing so. It shouldn’t be forgotten that during the period from 1795 to 1933 when the United States minted gold coins, there were constant political battles over the Gold Standard and its consequences. Whether it was how the new United States dealt with the debts incurred by the Continental Congress, the creation of or abandonment of the First and Second Banks of the United States, controlling or encouraging Free Banking, abandoning the convertibility of Gold in the 1860s and returning to the Gold Standard in the 1870s, the arguments over Bimetallism and William Jennings Bryan’s Cross of Gold in the 1890s, or how and whether to maintain the Gold Standard after World War I, returning to the Gold Standard would not

eliminate the political debate, it would just shift the debate to a different set of arguments.

Nevertheless, a majority of elected officials at both the Federal and State levels would have to be elected who supported implementing, then maintaining the new Gold Standard. Of course, this only begs the question because in order for Gold-Standard Politicians to exist, we would need a Gold Standard electorate who are willing to vote for politicians who support a new Gold Standard and against politicians who oppose it. This leads to the final step.

STEP 5. ACCEPT THE COSTS AND CONSEQUENCES OF A NEW GOLD STANDARD

At no point in America’s past did everyone support the Gold Standard. There were always people who were opposed to the Gold Standard because of the costs of deflation and tight money that come with the Gold Standard, and there were always those who supported the Gold Standard for the monetary stability that it provided. If America wants to return to the Gold Standard, the electorate needs to ask itself whether it is willing to accept the costs as well as the benefits of returning to the Gold Standard.

The primary cost is subjugating monetary and fiscal policy to maintaining the Gold Standard and accepting the responsibility that goes along with that decision because there would be real costs. Many of these costs were discussed above. There are no free lunches, even with a Gold Standard.

For monetary policy, returning to the Gold Standard means using higher interest rates and deflation as a way of maintaining the fixed price of gold, even during a recession. This also means maintaining the Fed’s independence to defend the Gold Standard against the short-run needs of politicians. If defending the Dollar’s link to gold means higher unemployment and slower growth, then so be it. Of course, supporters of the new Gold Standard would argue that in the long run, the monetary benefits of abandoning a fiat currency and maintaining a link to gold would offset these short-run costs, but that is a judgment the United States as a whole would have to make.

For fiscal policy, returning to the Gold Standard would mean subjugating Federal Government spending and taxing to maintaining a balanced budget that would enable the United States to maintain the Dollar’s link to gold. Any deficit in the current fiscal year would need to be offset by surpluses in the future. If unexpected expenses, such as a war occurred, the electorate would have to accept higher taxes. There would have to be caps on Entitlements such as Social Security, Medicare and Medicaid. This could mean raising the retirement age, cutting social security benefits, introducing means testing, requiring medical co-pays, capping the amount spent by Medicare on any individual or introducing other measures that would limit the amount the government spends on entitlements as a share of GDP. The Federal Government could no longer bail out the public and private sector. Transfers from the Federal Government to states and municipalities would have to be severely limited and unfunded emergency

requests for funds would have to be ignored. If a corporation or bank was in trouble, they would fail.

If this is what the electorate wants and the United States can put maintaining a Gold Standard and its benefits above the costs a new Gold Standard would incur, then they will elect politicians who will implement these changes. If the electorate feels the cost-benefit tradeoffs of a fiat currency with inflation, large redistributions and transfers through entitlements and bailouts, a depreciating currency, intervention in the economy from fiscal and monetary policy, government deficits, and everything else that comes with a fiat currency is better than the consequences of reintroducing the Gold Standard, they will stick with the current system. The important thing is that people understand the costs and benefits of each monetary system and choose the one that maximizes the benefits to the majority of people in the country.

WHICH CAME FIRST, THE GOOSE OR THE GOLDEN EGG?

Did the Gold Standard produce the fiscal and monetary restraint that occurred during the 1800s, or did the fiscal and monetary restraint of the 1800s enable the Gold Standard to exist. Which came first, the Goose or the Golden Egg?

Can the United States return to the Gold Standard? Absolutely. Is the Gold Standard a relic of the past that can never be reintroduced? No. Are there both costs and benefits of returning to the Gold Standard? Absolutely. Should we return to the Gold Standard? That is up to the electorate.

Even if the United States decided to return to the Gold Standard, it would be difficult for the US to return to the Gold Standard by itself. The Gold Standard was an international system that the largest countries of the world shared. There were alternatives. Countries could adhere to silver, which was more inflationary, or they could temporarily withdraw from the Gold Standard when war forced the country to use a fiat currency, but the Gold Standard of the late 1800s grew out of the minting of gold coins and the convertibility of government obligations into gold.

For one country to return to the Gold Standard while all others continue to use a fiat currency would be chaotic and would probably fail as the United States tried to control the value of gold against the rest of the world. And given the United States’ current level of debt, this would prove especially difficult. The United States would need to pay down its debt and build up reserves before it would be able to defend its Gold Standard against the rest of the world. To say the least, the United States is not currently in this position. For this reason, any return to a Gold Standard would probably have to part of an integrated international effort, not the action of a single country.

To actually return to the Gold Standard, the five steps listed above would have to be taken in reverse order. First, the electorate would have to decide that the Gold Standard is preferable to fiat currency, then the electorate would choose politicians who can put the Gold Standard into place. The politicians would have to pass bills to ensure a balanced budget in the future and change the directive of the Fed to defending the new Gold Standard. Then once that was in place, they could fix the price of the US Dollar to gold.

If the government were to enact the first four steps, returning to the Gold Standard would be a simple matter. In a way, it might even be superfluous. Most people who argue for a return to the Gold Standard do so because it would constrain the government’s ability to use fiscal and monetary policy to manipulate the economy and produce bubbles, but it isn’t the introduction of the Gold Standard which creates stable economic conditions, it is the fiscal and monetary policy needed to maintain the Gold Standard that provides stability. Despite the benefits of the Gold Standard during the 19th Century, when the Civil War occurred in the United States or World War I in Europe, countries went off the gold

standard because they had to.

To reiterate, it is the constraints the government places on fiscal and monetary policy that enables the government to adhere to the Gold Standard, not vice versa. Even if linking the U.S. Dollar directly to gold in a world where no other country is on the Gold Standard is difficult to do, there is no reason why the policies needed to maintain a Gold Standard cannot be introduced or enacted, regardless of whether the country actually reintroduces the Gold Standard.

The key to maintaining a Gold Standard without the Gold is that there be legal restraints on the government to prevent them from carrying out the Bubble policies of the past few decades. Passing a constitutional amendment to balance the budget or Congressionally changing the directive of the Fed might meet this purpose. Nevertheless, some people may feel that only the actual link to gold would ensure stable monetary policies and constraints on government activism.

Both the Gold Standard and a fiat currency have their costs and benefits. Those who advocate returning to a Gold Standard rarely describe the consequences and the costs of doing so. Unfortunately, both sides spend more time attacking each other than laying out the trade offs, costs and benefits of once again making Gold the basis of the American economy. Perhaps we haven’t reached the point where the electorate feels the cost of a fiat currency are great enough to justify abandoning it for Gold, or perhaps we have.

If the United States were to reintroduce the Gold Standard in a world in which no other country was on the Gold Standard, the action would probably fail. Nevertheless, this doesn’t prevent the United States from introducing the monetary and financial policies that would be necessary to maintain adherence to a Gold Standard. The real question is whether the United States has the political will to make these changes. Currently, it does not, but if talk of returning to the Gold Standard increases, it is important that people fully understand all the repercussions of returning to the Gold Standard. Only then they can make the political decision required to return to Gold.