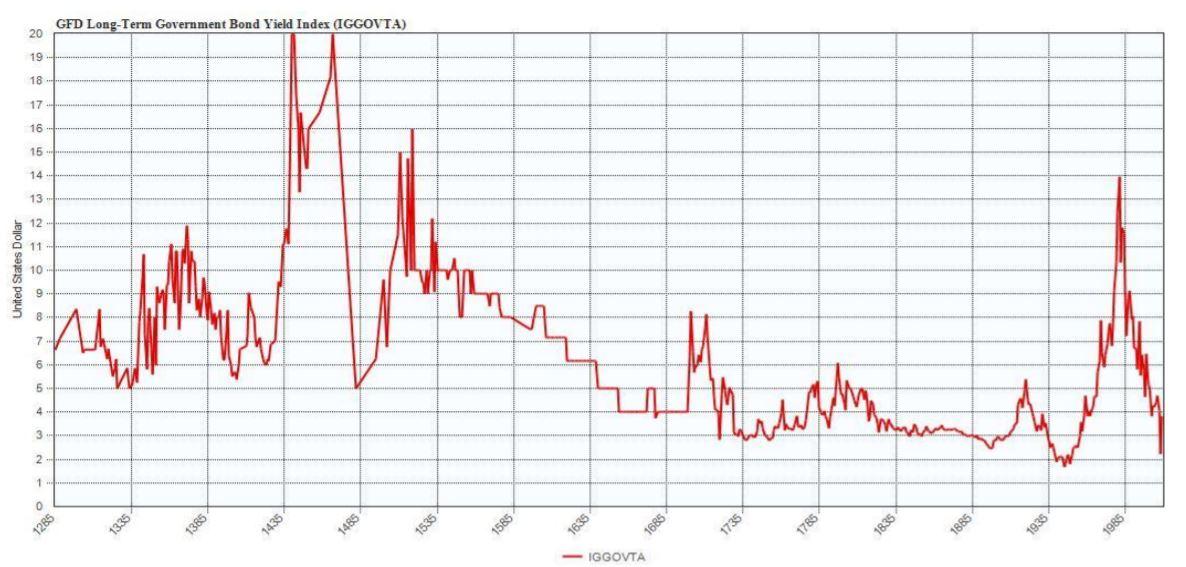

Global Financial Data has put together an index of government bond yields stretching back seven centuries. This index uses government bond yields from the leading economic powers of each century to measure the long-term changes in government bond yields.

The Changing Center of Financial Power

Over the past eight centuries, the locus of economic power has gradually shifted from Italy to Spain to the Netherlands to Great Britain and currently to the United States. The country at the center of the world’s power and economy issues bonds to cover expenses. Investors in that country and abroad purchase the bonds because they represent the safest bonds that are available for investment. The country at the center of economic power can issue more bonds at a lower cost because of the lower risk of the world’s economic center. Over time, power ebbs away from that country and investors begin placing their money in the bonds of the new world economic power. Italy was the center of the western economic world until the 1500s. Until then, the Mediterranean was the gateway to Byzantium, the Middle East, and through those countries, to India and China. The Italian city-states of Venice, Genoa, Florence and others grew from this trade, but also fought wars against each other requiring funds for those wars. By the 1600s, the nexus of economic power had shifted to the Netherlands as trade in the Atlantic and with northern Europe enabled the Dutch to strengthen their role in the global economy. The surplus of capital in the Netherlands is illustrated by the fact that Tulipmania, the world’s first bubble, which occurred in the Netherlands in the 1630s. The Netherlands was too small to maintain its role as the center of the global economy for long, and the combination of trade, and commercial and industrial revolutions moved the center of economic power to Great Britain at the end of the 1600s. The Glorious Revolution of 1688 realigned political power in England and put Britain on a sound economic footing that enabled it to remain the center of world economic and political power until 1914. After World War I, the center of economic power clearly shifted from London to New York and today, New York remains the center of the global economy. The Dollar is the world’s reserve currency, a fact that enables Washington to issue bonds at a lower cost than would otherwise be the case.

GFD’s Index of Government Bonds

Global Financial Data has put together an index of Government Bond yields that uses bonds from each of these centers of economic power over time to trace the course of interest rates over the past seven centuries. From 1285 to 1600, Italian bonds are used. Data are available for the Prestiti of Venice from 1285 to 1303 and from 1408 to 1500 while data from 1304 to 1407 use the Consolidated Bonds of Genoa and the Juros of Italy from 1520 to 1598. General Government Bonds from the Netherlands are used from 1606 to 1699. Yields from Britain are used from 1700 to 1914, using yields on Million Bank stock (which invested in government securities) from 1700 to 1728 and British Consols from 1729 to 1918. From 1919 to date, the yield on US 10-year bond is used.

Bond Yields Over Time

Bond yields are determined by a number of factors. These include 1) the growth in real GDP, 2) the inflation rate, 3) supply and demand factors, and 4) risk. The yield on a risk-free government bond should equal the growth in nominal GDP since that represents the opportunity cost of holding a government bond both in terms of investment opportunities (real GDP) and the time value of money (inflation). Higher levels of growth or higher inflation will lead to higher interest rates. Increases in the number of bonds (demand for savings) will lead to higher interest rates, while increases in savings will lead to lower interest rates. Finally, the perceived riskiness of the bonds can lead to higher interest rates. Investors may fear that the government may fail to pay back the bonds, reduce the real cost of the bonds through inflation, or depreciate the currency as a way of reducing their cost. All of these factors can impact the price of Government Bonds, and thus their yield. The trend over the past seven centuries has been for bond yields to decline. This can’t be attributed to lower economic growth or lower inflation, but must clearly be attributed to lower risk of default. Between 1285 and the mid-1600s, yields on government bonds fluctuated between 6% and 10% and in some cases were around 20%. Because there is little data on government bond yields before the 1700s, the spikes in yields that occur can be attributed to specific events that affected the issuers, generally the risk of default stemming from wars that occurred. It may very well be that yields on other securities were lower at different points in time up to the 1700s, but the paucity of data makes it difficult to determine this. Nevertheless, the trend is clear. Since 1700, well developed markets for bonds have existed in London and New York enabling the yields on government bonds to be traced with accuracy. Since the mid-1600s, the average yield on government bonds has been around 4%. Before the 1600s, high interest rates were driven by risk; since the 1600s, high interest rates have been driven by inflation. Being the center of economic power provides benefits to that country because it can issue bonds at a lower cost than a country in the periphery. In the long run, this can lead to over issuance of debt if the country chooses to take advantage of its position by issuing excessive debt to investors in other countries. With the mushrooming US government debt, some people are beginning to wonder whether the United States will be able to maintain its position as the world’s central economic power. Before looking at the United States, let’s look at government bond yields in Italy, the Netherlands and Great Britain in the past.

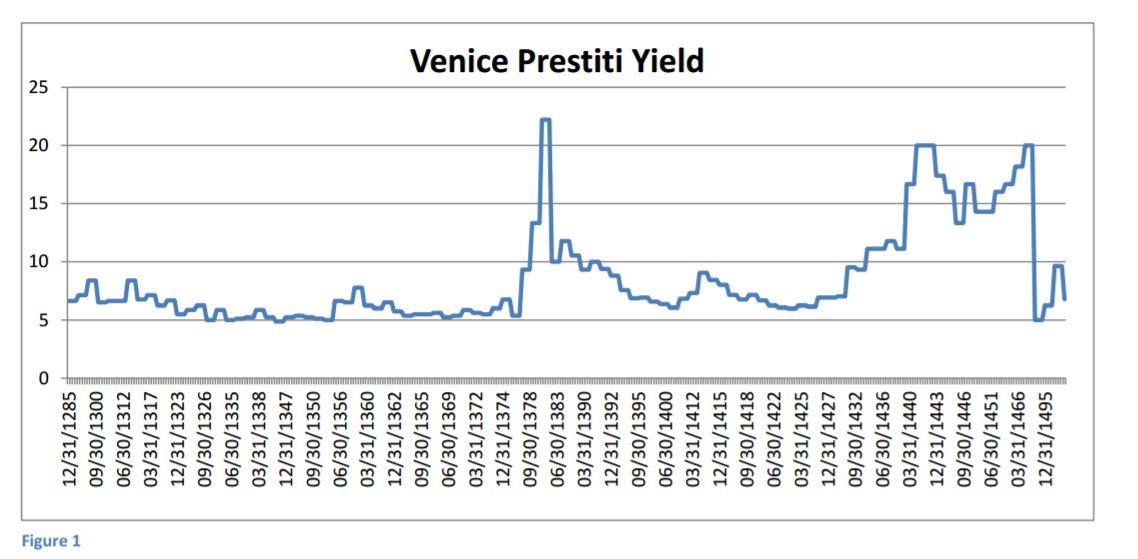

Italian Bond Yields

Because of the paucity of data from before 1700, bond yields as given in Sidney Homer’s A History of Interest Rates, are used. The two principal sources are the Prestiti of Venice (Figure 1) and the Consolidated Bonds of Genoa. During Medieval times, governments used taxes on trade and revenues from monopolies, on salt for example, to cover expenses during regular times, but inevitably wars broke out leading to the need to raise additional money. The government would have to find some way to force nobles and businessmen to hand over money to cover the costs of war.

Genoa and Venice used “forced loans” as a way of raising funds from its citizens. The two citystates consolidated these forced loans and allowed creditors to trade these forced loans on open markets turning them into modern-day bonds. The debts had no maturity date, but during periods of peace, the governments would use surplus revenues to retire some of these debts.

Governments that met interest payments on their forced loans, paid off debts during peace times, and did not default on these debts could establish confidence in their debt, enabling them to issue more bonds in the future. As Venice prospered, it increased its ability to service its loans. Venice established a fund to repurchase Prestiti, floated voluntary loans when necessary, borrowed in anticipation of future tax collections, and established a credible record of repayment. This enabled the cities of Venice and Genoa to borrow money at 6%-10% during Medieval times and during the Renaissance, rather than the 10%-15% that other rulers had to pay.

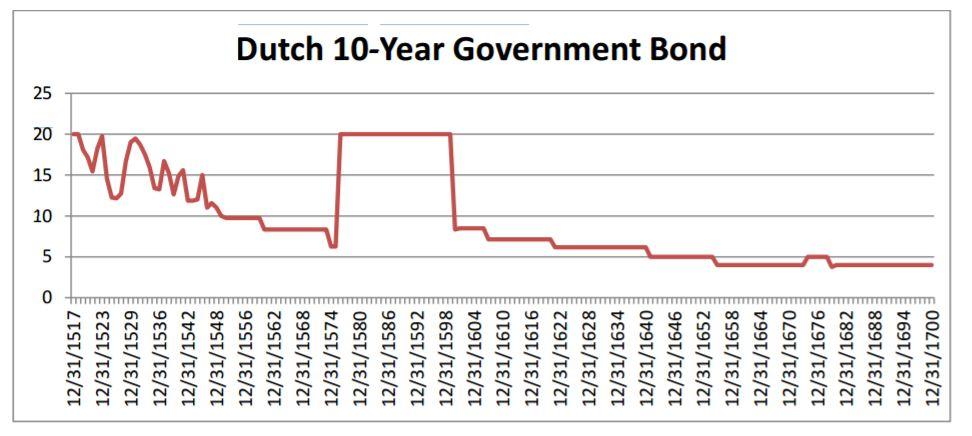

Dutch Bond Yields

As the center of trade shifted out of the Mediterranean and into the Atlantic after 1500, the center of economic power shifted as well. The rulers of Spain, France and England had periodically defaulted or forced loans on their subjects, and failed to establish a record of regular repayment of loans that would have enabled them to become the financial centers of Europe.

The Netherlands successfully liberated itself from Spain between 1568 and 1648. The Dutch established the Dutch east India Company in 1602 and the Dutch West India Company in 1621. The Netherlands didn’t have to pay for an expensive court, fought their wars at home rather than abroad, profited from international trade, and saved money. The Amsterdam Exchange dealt not only in shares of the Dutch East India Company and Dutch West India Company, but in government bonds as well.

Outside of the Italian city-states, loans to heads of state were basically personal loans that clearly ran the risk of default. Spanish, French and English kings borrowed when they had to, defaulted when they couldn’t pay, but had no system of drawing upon the savings of the public. The Dutch, on the other hand, developed state finance based upon the government’s ability to pledge its revenues against the annuities they had issued. Having no royal court, and relying upon local governments, the Dutch paid off loans on time with little risk of default. As risk declined, interest rates fell to 4% (Figure 2), the lowest they had ever been in history and a rate consistent with the low level of default risk that governments enjoy today.

English Government Bond Yields

The Glorious Revolution of 1688 transformed England politically and economically. Unlike his predecessors, William III was a constitutional monarch. Though he had no pretensions to absolute personal power, and though in theory he borrowed on behalf of the English people, he also represented the Whig mercantile interests which backed him and dominated Parliament. The Bank of England was established in 1694, borrowing at 8% (when Dutch rates were at 3-4%), and in 1720, the attempt to convert existing government debt into shares in the South Sea Company created the South Sea Bubble. By the 1740s, interest rates had declined to the 3% range and in 1751 the 3% British Consols were issued, which are still traded in London today.

As can be seen by the graph of long-term interest rates, the risk of default on British debt has been almost non-existent as illustrated by the consistently low interest rates, except in time of inflation. During the Napoleonic Wars, Britain’s Government debt as a share of GDP exceeded 200%, but government bond yields stayed below 6%. After 1815, British capital funded canals, railroads in the UK, America and other countries, mines in Latin American, Britain’s colonies and foreign bonds issued by every government in the world. Since there were no major wars or fiscal crises in the UK after 1815, Britain’s Government debt shrank to 20% of GDP by 1914. Interest rates on government bonds fell below 2.5% in 1896, enabling Britain to reduce the interest rate on its Consols to 2.5%.

Other countries also benefited from the decline in interest rates. The United States, Germany, France and other countries were all able to issue government debt at 3% by the end of the 1800s, whereas at the beginning of the 1800s, 5-6% or even more was the norm. Small government, due to few or small wars, combined with shrinking government debt reduced the risk of default and lowered interest rates throughout the world.

United States Bond Yields

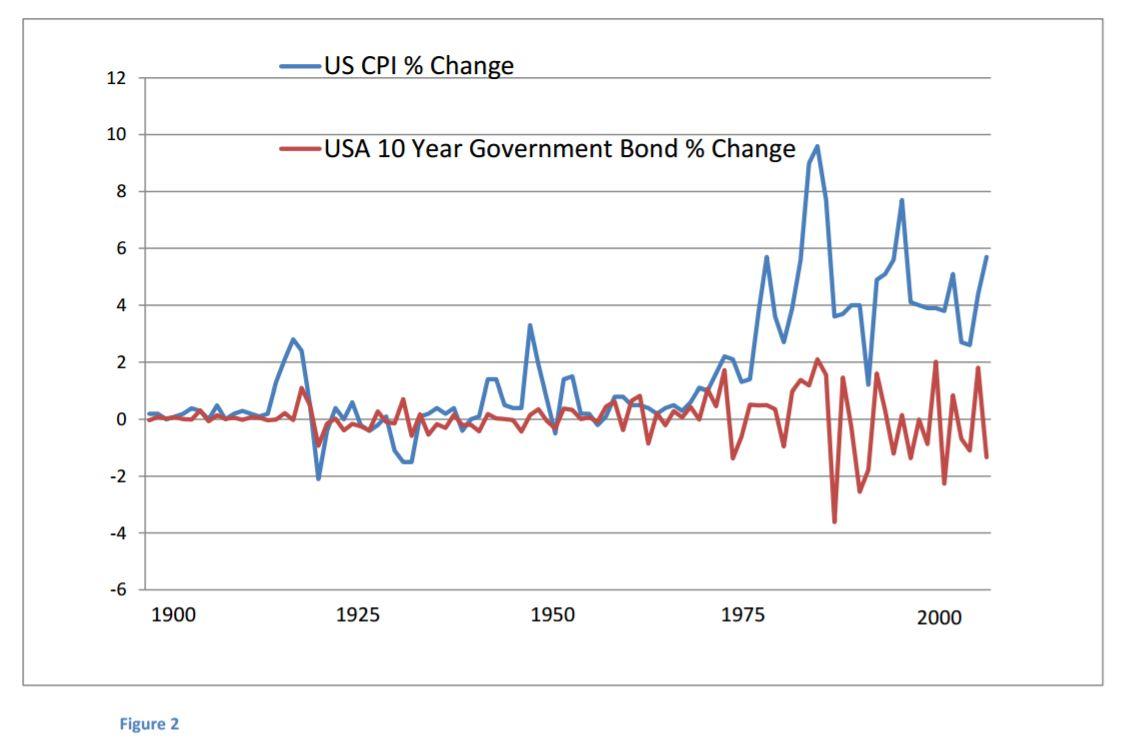

World War I shifted the world’s financial center from London to New York. In 1915, British bond yields rose above American yields and have remained that way ever since. The United States has never defaulted on its Central government bonds, so rises in bond yields have been driven mainly by higher rates of economic growth, inflation, and the supply and demand for government bonds.

There are several clear trends in government bonds in the US during the past 100 years. From 1902 to 1920, bond yields rose from 2.82% to 5.67%, with most of the increase occurring between 1914 and 1920 due to the risks of war and inflation. From 1921 to 1945, interest rates fell from 5.67% to 1.55% due to deflation, depression and the manipulation of bond yields during World War II by the government. From 1945 to 1981, interest rates rose from 1.55% to 15.84%. This was the highest level for government bond yields in almost 500 years as inflation spiraled out of control due to Keynesian economic policies. Between 1981 and 2011, bond yields fell from 15.85% to 1.46%.

Bond Yields in the Twenty-First Century

What will this chart look like at the end of the 21st century? The clear driving factor for bond yields over the past seven centuries has been the responsibility or irresponsibility of national governments. From Venice and Genoa to the Netherlands, Britain and the United States, when governments kept borrowing to a minimum and paid off their debts, interest rates fell, benefitting not only the national, but the global economy. Capital was freed up for the private sector which contributed to the success of the industrial revolution. The 1700s and 1800s had the lowest interest rates in history. The 1900s enjoyed both some of the lowest and the highest interest rates (Figure 3), depending upon the level of inflation generated by the government. Since the risk of default is low, it is inflation and the supply and demand for bonds that has driven interest rates since the mid-1700s.

Government bond yields reached their lowest levels in history in 2012, dropping below 1.50%. Whether bond yields start to rise from here will depend upon the behavior of the government and its willingness to balance its books. US government debt has increased to over 100% of GDP. This is no guarantee that interest rates will rise since investors flee to US Government Debt as a haven of safety. Britain’s debt exceeded 200% of GDP after the Napoleonic Wars and Japan has run deficits for 20 years with its government debt edging toward 200% of GDP.

Nevertheless, Britain paid off its debt during the 1800s keeping interest rates from rising. Japan has seen no growth in nominal GDP during the past 20 years, and has been able to rely upon domestic savings to fund its growing government debt. Currently, there is no prospect that the United States will begin to pay off its debt as Britain did in the 1800s, and low interest rates are little consolation if your economy is not growing. When the economy returns to more normal growth rates and the rest of the world becomes less risky, government bond yields will rise.

Even if the United States were to suffer the fate of Japan and fail to grow for the next 20 years, which is unlikely, its inability to fund its debt domestically, and the inevitable growth of China, India and other emerging markets, is likely to drive growth and interest rates upward in the decades to come. Although the United States may not default on its debt, it can reduce the burden through inflation or depreciation. If this were to occur, the balance of financial power could shift again. Whether United States bond yields are used in this graph at the end of the 21st Century, or those of China, India or some other country will depend upon the fiscal constraint or profligacy of the US Government.

As long as investors perceive that the United States remains the center of the world’s economy with little risk of default, the United States can continue to benefit from low government bond yields, but if US government debt continues to grow and another economic center develops which is perceived as being safer than the United States, the US could lose its role as the center of the global economy and all the benefits that go with it.