Yields on United States 10-year bonds passed the 3% in January. The yield on the 10-year had reached its lowest point in history in 2012 at 1.43% as a result of the Fed’s policy of Quantitative Easing. Since then yields have doubled as the markets incorporated the impact of tapering their purchase of U.S. Government securities.

This raises the question, how high could interest rates go from here? Could interest rates move up to 3% per quarter? U.S. interest rates were that high back in 1981 when the yield on US 10-year Treasuries 15.84% while 30-year mortgage rates hit 18.63%. What about 3% per month, per week, or even per day?

HYPERINFLATION AS THE NEW NORMAL

Brazil was one of the worst of the Latin American hyperinflators of the 1960s to 1990s. New currencies were introduced in 1967, 1986, 1989, 1990, 1993 and 1994. The Real, introduced on July 1, 1994, put an end to Brazil’s addiction to inflation, but by the time the Real was introduced, the new currency, was equal to 2.75 Quintillion (2,750,000,000,000,000,000) Reis, the original currency Brazil had used as a Portuguese colony. The impact of these inflations on the currency is illustrated below in the log chart of exchange rates between the Brazilian currency and the US Dollar from 1950 to 2014.

The Banco do Brazil uses the SELIC (Sistema Especial de Liquidação e Custodia – Special Clearance and Escrow System) to set interest rates for the economy, just as the Federal Reserve uses the Discount rate in the United States. The SELIC became the basis for all interest rates throughout the Brazilian economy as hyperinflation took over. At first the SELIC was adjusted every few years, then every few months, then daily. Along with the exchange rate for the SELIC became the primary indicator of inflation on the Brazilian economy.

What is most interesting about the graph is the exponential increase in interest rates from 1975 to 1993, rising steadily from around 16% per annum to almost 16,000% until the back of inflation was broken in 1993. Currency reforms are visible in the large drops in the interest rate as the government tried to reform the fiscal sector and stop the inflationary spiral, but the government inevitably returned to its inflationary fix to solve its problems.

HOW TO BANKRUPT BORROWERS

Although 3% may not seem like a lot, compounding that on a daily basis adds up very quickly. If you take the 30 days from February 1 to March 2, 1990, the product of these interest rates comes to 167% in one month (inflation was 75.7% in February 1990). If you extrapolate that on an annual basis, interest rates in Brazil hit a high of 790,799% on February 19, 1990. In other words, if you had borrowed $100 on February 19, 1990, you would have owed the bank $790,799 a year later. Payday loans sound cheap by comparison. Obviously, this situation was unsustainable. The newly elected President, Fernando Affonso Collor de Mello, introduced his “shock” plan to cure the economy on March 16, 1990, closing banks for three days, the Novo Cruzado replaced the Cruzeiro, and 20% of overnight market funds were frozen for 18 months. A 30-day wage and price freeze, a new wealth tax, and a widening of the tax base were introduced. Although the currency reform slowed the rate of inflation, decreasing it from a monthly rate of 82% (135,000% annually) in March 1990 to 7.6% by May (140% annually), inflation picked up from there. Monthly inflation began its steady increase as the government continued to print Cruzeiros rather than raise taxes. Monthly inflation steadily increased to 47% by June 1994 when the introduction of the Real put an end to Brazil’s hyperinflation. Though the United States is unlikely to go the route of Brazil, it does show what can happen when quantitative easing becomes too easy. Yields on United States 10-year bonds rose above 3% at the beginning of January 2014. The yield on the 10-year had reached its lowest point in history in July 2012 at 1.43% as a result of the Fed’s policy of Quantitative Easing. Since then yields have doubled as markets have incorporated expectations of Fed tapering the purchase of U.S. Government securities.

Yields on United States 10-year bonds rose above 3% at the beginning of January 2014. The yield on the 10-year had reached its lowest point in history in July 2012 at 1.43% as a result of the Fed’s policy of Quantitative Easing. Since then yields have doubled as markets have incorporated expectations of Fed tapering the purchase of U.S. Government securities.

$12,000 Mortgage Payments Anyone?

What will happen in the United States when tapering and quantitative easing come to an end? How high could interest rates rise? Could interest rates move up from 3% per annum to 3% per quarter, revisiting the levels of 1981? When the yield on US 10-year Treasuries hit 15.84% in 1981, as seen in the chart below, mortgage rates hit 18.63%. And it was not uncommon during this time for home loans to be as high as 20%! Imagine a 20% APR on your mortgage. This would make a standard $3,000 monthly payment of 2014 rise to $12,000 per month. There are eerie parallels today with the experience of World War II when the yield on US 10-year bonds also fell below 3%. Bond yields had fallen below 3% in 1933 as a consequence of the Great Depression, but the government kept interest rates below 3% until the 1950s to reduce the cost of funding World War II. The Treasury pledged to keep the interest rate on Treasury bills at 0.375% or below while the United States was at war. Interest rate repression is nothing new for the Fed.

The problem with the Fed’s World War II policies was that interest rate repression eventually led to inflation of 14% in 1947 and 8% in 1948, making real interest rates negative. To stop this, the Fed put pressure on the Treasury to allow interest rates to rise to their market level, which the Treasury finally did in 1951. As you can see in the graph above, interest rates rose for the next thirty years.

The ABCs of HyperINFLATION

Interest rates at these levels can only occur because of inflation. The problem is that as inflation rates rise, bond yields become more unstable and unpredictable. Consequently, the maturity of debt instruments shrinks as uncertainty increases. Annual interest rates become meaningless, and the maturity of debt shrinks to months, weeks, days or in extreme cases, even hours.

Interest rates even hit 3% per week in Germany during its hyperinflation. In 1923, the interest rate charged at the Berlin Stock Exchange in October 1923 hit a high of 7950%, the equivalent of 9% per week. One of the worst cases was Brazil in 1990 when interest rates hit over 3% per day!

We are about half way through January and many analysts, investors and market enthusiasts are wondering which way that markets are headed. Typically, the markets go through the “January Effect” which is a general increase in stock prices during the month of January. This rally is generally attributed to an increase in buying, which follows the drop in price that typically happens in December when investors, seeking to create tax losses to offset capital gains, prompt a sell-off. For 2014, this move has been less evident, as a matter of fact, the markets have been flat for the US and Europe (expect Greece) where as Asia has been down. What is going this January? Could it be that many investors are re-balancing their portfolios by selling part of their profits from 2013 in stock and re-allocating the proceeds to bonds? January is a common time for re-balancing and tax harvesting. The S&P 500 gave us about 30% returns in 2013 and profit taking is common to lock in some of those gains. Will 2014 bring us similar returns to 2013?

We are about half way through January and many analysts, investors and market enthusiasts are wondering which way that markets are headed. Typically, the markets go through the “January Effect” which is a general increase in stock prices during the month of January. This rally is generally attributed to an increase in buying, which follows the drop in price that typically happens in December when investors, seeking to create tax losses to offset capital gains, prompt a sell-off. For 2014, this move has been less evident, as a matter of fact, the markets have been flat for the US and Europe (expect Greece) where as Asia has been down. What is going this January? Could it be that many investors are re-balancing their portfolios by selling part of their profits from 2013 in stock and re-allocating the proceeds to bonds? January is a common time for re-balancing and tax harvesting. The S&P 500 gave us about 30% returns in 2013 and profit taking is common to lock in some of those gains. Will 2014 bring us similar returns to 2013?

The new US $100 bill is out, as you may have seen this holiday season. Our dear old Uncle Ben is a technological wonder with a dozen different anti-counterfeiting devices on it. Since there are more $100 bills circulating outside of the United States than inside, the U.S. Government has to insure that counterfeiters are unable to replicate the government’s most treasured export. This raises the question, who was the greatest counterfeiter of all time?

The new US $100 bill is out, as you may have seen this holiday season. Our dear old Uncle Ben is a technological wonder with a dozen different anti-counterfeiting devices on it. Since there are more $100 bills circulating outside of the United States than inside, the U.S. Government has to insure that counterfeiters are unable to replicate the government’s most treasured export. This raises the question, who was the greatest counterfeiter of all time?

Government Counterfeiting

- The Roman Empire replacing its silver Denarii with billon Antonininii;

- The Khans of China creating the first paper inflation in the 1300s;

- The United States making its first currency, the Continental Dollar, worthless;

- Germany hyperinflating out of its debts by creating trillions of marks;

- Or the US Federal Reserve blowing up its balance sheet.

- Barbarians did of the Roman gold Aureus

- British did of Continental Dollars and French Assignats during the 1700s

- Germans did of British Pounds during World War II in Operation Bernhard

- United States did of Japan’s Occupation currency of the Philippines

- North Koreans did of US Dollars, making them one of their principle exports.

A Classy Counterfeiter

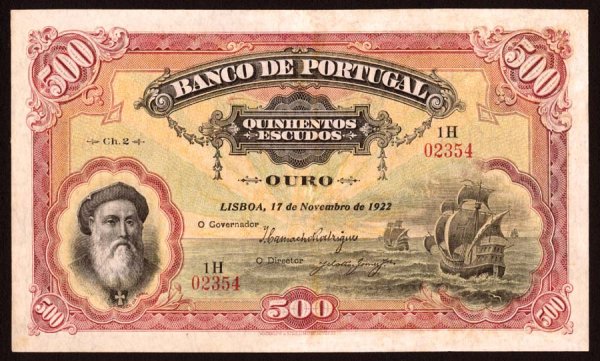

Our vote for the greatest counterfeiter of all time goes to Artur Alves dos Reis whose story was recounted by Murray Teigh Bloom in The Man Who Stole Portugal. Reis was both smart and classy, and his criminal operation reflected these qualities. To my knowledge, Reis put together the most audacious counterfeiting scheme in history. He conceived his master plan while he was in jail in Oporto for embezzling the funds of a company he had taken over. Some criminals sit in jail and try to avoid repeating their misfortunes. Others, like Reis or Tony de Angelis, think-up bigger, more foolproof schemes. While he was sitting in his cell, Reis put together his master plan that would make him the richest, and possibly the most influential man in Portugal in only one year.Although you may not realize it, counterfeiting is a very complex operation. To be successful, (i.e. not get caught), be able to spend your money, and not receive free room and board from the government, you have to do three things successfully. First, you have to create counterfeit currency that can’t be detected. Second, you need a way of laundering the money and converting it into real assets so you can enjoy the fruits of your ill-begotten labors. Third, you must make sure that you avoid the triple curse of detection, arrest and conviction. Let’s see what Reis’s solution was to this age-old problem.Step One: Create an Undetectable Banknote

First, create a counterfeit that can’t be detected. During the 1920s, the Banco do Portugal had the exclusive right to print currency in Portugal. The bank used foreign printing companies with superior anti-counterfeiting technology to protect their banknotes. The English company, Waterlow & Sons, printed the 500 and 1000 Escudo notes (equal to about $25 and $50 in 1923) for the Banco do Portugal. So why not get Waterlow & Sons to print the notes for Reis as well?Reis was a natural-born forger. He forged his diploma as an engineer from Oxford as a “joke”, but this helped land him a job as a government railroad inspector in Angola at the age of twenty-two. In 1924, he forged $100,000 worth of checks and used the money to take over control of Ambaca, the Royal Trans-African railway Company of Angola. He then used the money in the company’s treasury to cover his own checks. He was arrested in July 1924 for embezzlement, but was released two months later when a court decided his was a civil and not a criminal case. It was during the two months he was the guest of the Oporto police that he conceived his infamous counterfeiting scheme. The key was to find someone with a respected name who could help him convince Waterlow & Sons to print banknotes secretly for Reis. He found three men of questionable repute, but with connections to help Reis: Jose Bandeira, Gustav Adolf Hennies and Karel Marang. Bandeira got his brother, the Portuguese Minister to the Netherlands, to give Marang a letter introducing him as a respected Dutch citizen who had a power-of-attorney for Alves Reis to negotiate the printing of the banknotes. Marang went to Waterlow & Sons in London, and presented his letter of introduction as the “Consul General of Persia” on forged Banco do Portugal stationary to Sir William Waterlow. Marang spun the story Reis had instructed him to give. A private syndicate was being formed to save the colony of Angola from its current dire financial condition with a $5,000,000 investment. In return for the loan, the syndicate would be allowed to print and circulate banknotes in Angola. Waterlow & Sons would print the banknotes for the syndicate, and once the notes reached Angola, the banknotes would be supercharged with the word ANGOLA so they wouldn’t be confused with notes from the mother country. The whole affair had to be kept secret lest Angola fall into further financial difficulties due to ill-placed rumors of pending economic ruin. Of course, Sir William knew that supercharging notes was normal practice for Portugal’s colonies, and that the Banco Ultramarino had the exclusive right to print banknotes for the Portuguese colonies. This was an opportunity for Waterlow & Sons to get this business away from Bradbury, Wilkinson & Co., the current printer of banknotes for the Banco Ultramarino in Angola. Marang asked Waterlow to print the 500 Escudo note with Vasco da Gama on it. The deal was signed on January 6, 1925, and for the printing cost of $7,200, Reis and his conspirators would receive $5,000,000 in banknotes, a 70,000 percent return on their investment. Bandeira picked up the first group of notes from Waterlow & Sons on February 10, and by March 20, they had 100 million Escudos ($5,000,000) in Portuguese banknotes. Bandeira used his orange diplomatic card to transport the bills in luggage marked the “Legation of Portugal” across the borders without detection. After the first step had been successfully completed, they placed an order for an additional 190 million Escudos in banknotes ($9,500,000). Of course, the banknotes never made it to Angola.

The greatest risk in the scheme was having banknotes with duplicate numbers discovered, but this was the lesser of two evils. If Reis and Marang had requested banknotes outside the numerical range of the 500 Escudo notes, the spurious notes would have been quickly discovered. The lower risk lay in duplicating the existing serial numbers, and hoping the counterfeiters were able to successfully release all the banknotes before the law of large numbers caught up with them.

Step Two: Laundering Money with Your Own Bank

Step One of the plan was complete, now for Step Two: laundering the money. A small-scale counterfeiter can pass bills through petty criminals, but the notes Reis and friends had were equal to almost 1% of Portugal’s GDP. This was the equivalent of over $150 billion if the same amount had been released in the United States today. Even if Reis hired every petty criminal in Lisbon and Oporto, he wouldn’t be able to unload a fraction of the banknotes.

Step Three: Avoid Detection (For a While)

Step Three and the most important of all was how to avoid detection, arrest and imprisonment. For this, Reis had a brilliant solution. Since they were counterfeiting Banco do Portugal banknotes, only the Bank could initiate proceedings to prosecute them. But what if –just what if– Reis controlled the shares in the Banco do Portugal? The bank had already exceeded its statutory banknote limit many times over and the directors of the Banco do Portugal had never been prosecuted, so why should they prosecute Reis? Or as Reis put it, “How can they arrest us when they’re us and we’re them?”Like most European countries, Portugal had suffered inflation after World War I. Prices had increased 48% per annum between 1919 and 1924, and the Escudo had depreciated by 87% against the Pound Sterling. Although the Banco do Portugal was only supposed to issue banknotes thrice its capital, it had, in fact, issued banknotes a hundred times its capital. By comparison with this, Reis’s monetary manipulations were minor by comparison. The chart below shows the depreciation of the Portuguese Escudo against the U.S. Dollar after World War I.