|

Dr. Bryan Taylor, President and Cheif Economist for Global Financial Data, speaks with KPCW, Mountain Money about the impacts the Spanish Flu had on the stock market in 1918 and how we can look at that data to understand the current market and impacts from COVID-19. |

[embed]https://cpa.ds.npr.org/kpcw/audio/2020/03/mm_03162020_dr_bryan_taylor.mp3[/embed]

https://www.kpcw.org/post/spanish-flu-and-stock-market-how-can-we-use-data-today#stream/0

Full Article

Everyone is concerned about the coronavirus and how it is impacting the global economy. Parts of China have been quarantined to prevent the spread of the virus and the world is wondering how the virus will disrupt supply chains between China and the rest of the world and how it will impact global travel. Will cities that are cut off from the rest of the world be able to contribute to the global economy?

The main precedent for the coronavirus is the SARS epidemic of 2002-2004, but you should also look at the more serious Spanish Flu pandemic of 1919. It is estimated that the Spanish Flu infected 500 million people worldwide, or about 27% of the world’s population and killed between 30 million and 50 million people, or about 1.7% of the world’s population. Were a similar pandemic to hit the world today, this would translate into 100 million deaths. This made the Spanish flu one of the deadliest epidemics in history. The pandemic occurred in the last year of World War I and military censors in France, Germany, the United Kingdom, United States and other countries were told to control information on the flu fearing that it would affect their ability to win the war, but there was no censorship on the flu in neutral Spain where King Alfonso XIII took ill. This gave the world the false impression that the flu originated in Spain, hence the name.

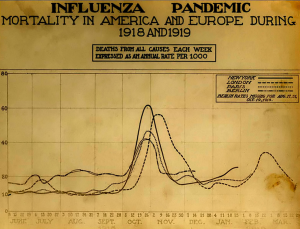

The Spanish flu came in three waves as is illustrated in Figure 1. The first wave, which made people notice the flu, occurred in July 1918. The second and most deadly wave occurred in October 1918 and resulted in millions of deaths. A final wave of the flu occurred in February 1919, and after that, the flu disappeared. Either the virus mutated to a less lethal form or doctors got better at treating or preventing it. Just as no one knows for sure exactly where the virus came from, no one knows why it disappeared.

Figure 1. Death Rates of the Spanish Flu, June 1918 to May 1919

It is interesting to contrast the response of the stock market to the Spanish flu in 1919 with the coronavirus in 2020. The Dow Jones Industrial Average fell over 2,000 points in four days out of fear that the coronavirus will continue to spread and impact the global economy. The fear is that cities will become quarantined, supply chains will be broken, world trade will be impacted and growth in the global economy will slow down.

However, the impact of the Spanish Flu on the stock market was minimal. If you look at the Dow Jones Industrial Average in 1918 and 1919, you can see that the stock market was relatively unaffected by any of the three waves of the Spanish flu. Of course, the Spanish flu occurred in 1918 while World War I was raging in Europe so the war had a larger impact on the stock market than the flu. There were few if any global supply chains that the Spanish Flu could disrupt because the war made supply chains nonexistent. The second and worst wave of flu occurred at the end of World War I when peace was finally achieved after four years of devastating destruction. It is interesting that there was little impact on the stock market of World War I ending on November 11, 1918. Perhaps euphoria about the conclusion of the war was offset by concerns about the Spanish flu.

It is comforting to see that when the final wave of the Spanish flu subsided in February 1919, the market began an increase of 50% which lasted until November of 1919. Whether this increase occurred because of the end of World War I or the end of the flu or both is impossible to say, but it does provide encouragement that once the coronavirus begins to subside, the market will bounce back once again.

The United States stock market has broken to new highs in January 2020, continuing a bull market that began in March 2009. The S&P 500 has risen 382% since March 2009 and is approaching the record bull market of 1974-1987 in which the S&P 500 rose 442%. This would be only the fourth time that an American bull market rose by more than 400% if this bull market continues. As Figure 1 shows, US stock market Capitalization is close to the same levels as in 1999 when the Internet Bubble burst. By our estimate, when the S&P 500 hits 3650, the stock market’s capitalization will be twice GDP.