Argentina is one of the most interesting countries among emerging markets. Argentina was one of the ten richest countries in the world in the 1920s, but now doesn’t even make the top 50. Argentina was downgraded from emerging market status by MSCI to being a frontier market in 2009 when President Cristina Fernandez imposed capital controls making it difficult for foreigners to invest. Mauricio Macri became the leader of Argentina in 2015 and worked to undo the financial harm that Cristina Fernandez had imposed on the country. Argentina was able to issue a 100-year bond in June 2017, but in 2018 the country went to the IMF for a $56 billion loan. MSCI will upgrade Argentina back to emerging market status in 2019, but its future remains uncertain. The trials and tribulations that Argentina’s leaders have put the economy through are reflected in the returns to investors over the past 150 years.

Argentina was settled by the Spanish, and a local government replaced the Spanish government in 1810. The Buenos Aires stock market was founded in 1854, and has operated for the past 165 years. After the Argentine federation was formed in 1860, Argentina enjoyed growth until 1930, relying upon agricultural exports to make it one of the ten richest countries in the world. The country grew faster than either Canada or Australia, but industry represented a small portion of output. Argentina shipped meat to Europe, taking advantage of the vast pampas where cattle were raised, but failed to develop a large manufacturing base.

In 1930, the military overthrew President Yrigoyen, and in 1946 Juan Domingo Perón gained power in Argentina and promoted the “three flags” of social justice, economic independence and political sovereignty. Before 1930, Argentina was one of the most stable countries in the world, but since 1930, it became one of the most unstable. Between Peronism, military dictatorship, hyperinflation and protectionism, Argentina suffered inconsistent economic policies that prevented the economy from growing quickly. As late as the 1960s, per capita income in Argentina exceeded that of Spain, Japan or Ireland. Today, Argentina’s per capita GDP is about $10,000 which places outside of the top 50 richest countries in the world. Quite a slide from being in the top 10 ninety years ago.

Argentina has defaulted on its debt eight times with recent defaults or restructurings in 2001, 2005, 2010 and 2014. Between 1944 and 1982, Argentina suffered annual inflation of 92% with triple-digit inflation in 15 of those years, and an inflation rate over 5,000% in 1989. The inflation rate today is 54%. The Peso was at parity with the U.S. Dollar between 1992 and 2001, but has collapsed since then. Today there are over 40 Pesos to the U.S. Dollar. Will Argentina ever be able to provide the economic stability it deserves?

Stock Market Returns

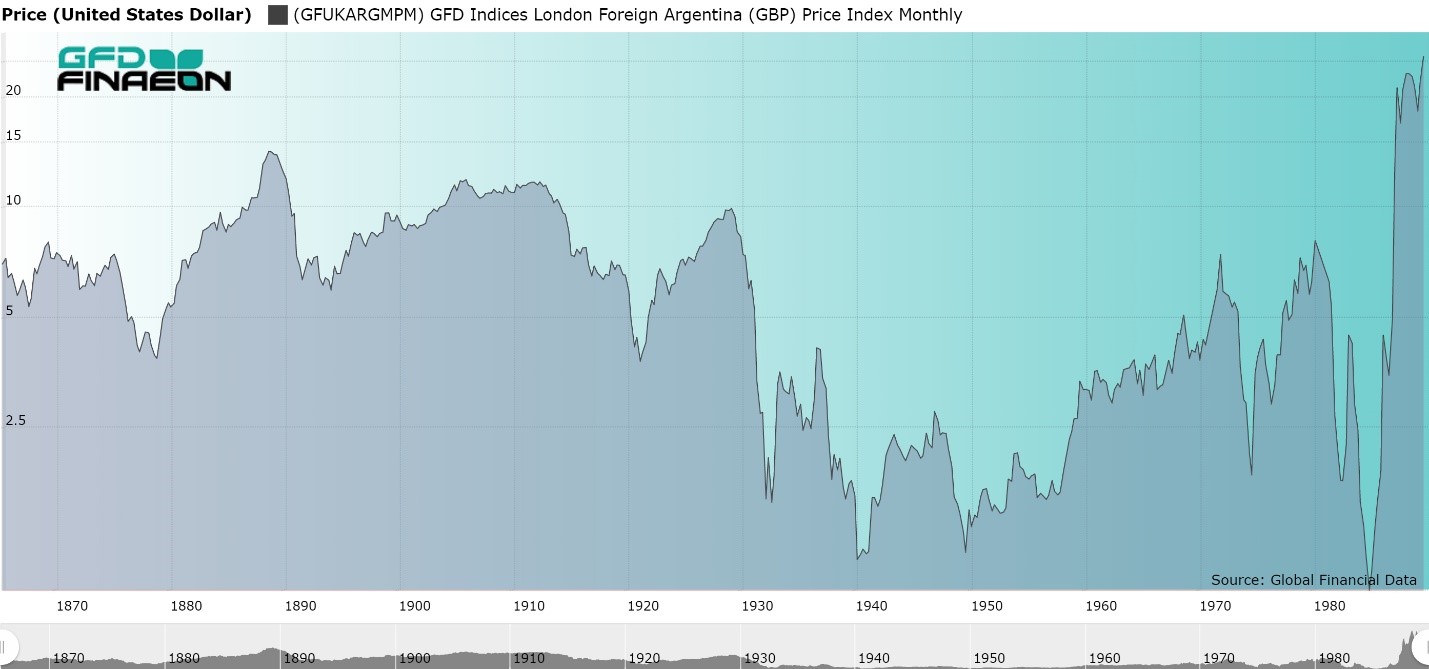

But how has Argentina’s stock market performed compared to the rest of the world? Argentine shares first listed in London in 1863 when the Buenos Aires Great Southern Railway issued shares. We can use data on Argentine shares in London to create an index of shares from 1865 until the 1960s. An Argentine brokerage firm, Swan, Culbertson and Fritz calculated a stock index between 1947 and 1958 with annual data calculated back to 1938 and the Buenos Aires stock exchange has calculated a daily index of shares since 1967. For the remaining years between 1865 and 1947 and between 1958 and 1967, we have used data from London as a proxy for Argentine shares.

Of the 55 companies that listed in London between 1865 and 1985, eight were consumer staples companies (mainly tobacco and food), five were finance, six were materials, five were real estate, nine were utilities and twenty were transports. The Buenos Aires Great Southern Railway had the longest life of any company that listed in London, lasting from 1863 until 1948 when Juan Perón nationalized Argentina’s railroads along with the Buenos Aires and Pacific Railway, the Buenos Aires Western Railway and the Central Argentine Railway. The performance of Argentine shares in London is illustrated in Figure 1. There was little change in the stock market between 1865 and 1929, but after the military overthrew the government in 1930, stocks collapsed.

Because the exchange rate is so volatile, the size of the stock market and returns as measured in US Dollars can vary widely. The stock market capitalization was over $700 million in 1929, but still only $800 million in 1977. Argentina’s stock market capitalization fell from $105 billion at the end of 2017 to $46 billion at the end of 2018. This was less than it had been in 1994 ($47 billion). With a market cap of $46 billion, Argentina’s stock market represents less than 10% of GDP. There is obviously room for growth if politicans can stabilize the economy.

Carlos Menem was elected president in May 1989, and ended up privatizing almost every company the state owned. On January 1, 1992, a currency board was introduced, linking the Argentine Peso directly to the U.S. Dollar. Anticipating the growth Menem’s reforms would generate for the economy, the stock market rose over 99% per annum between 1987 and 1991. The next few years were ones of growth in the economy; however, in 2002 Argentina was unable to maintain its link to the U.S. Dollar, and the economy faced a decade of instability.

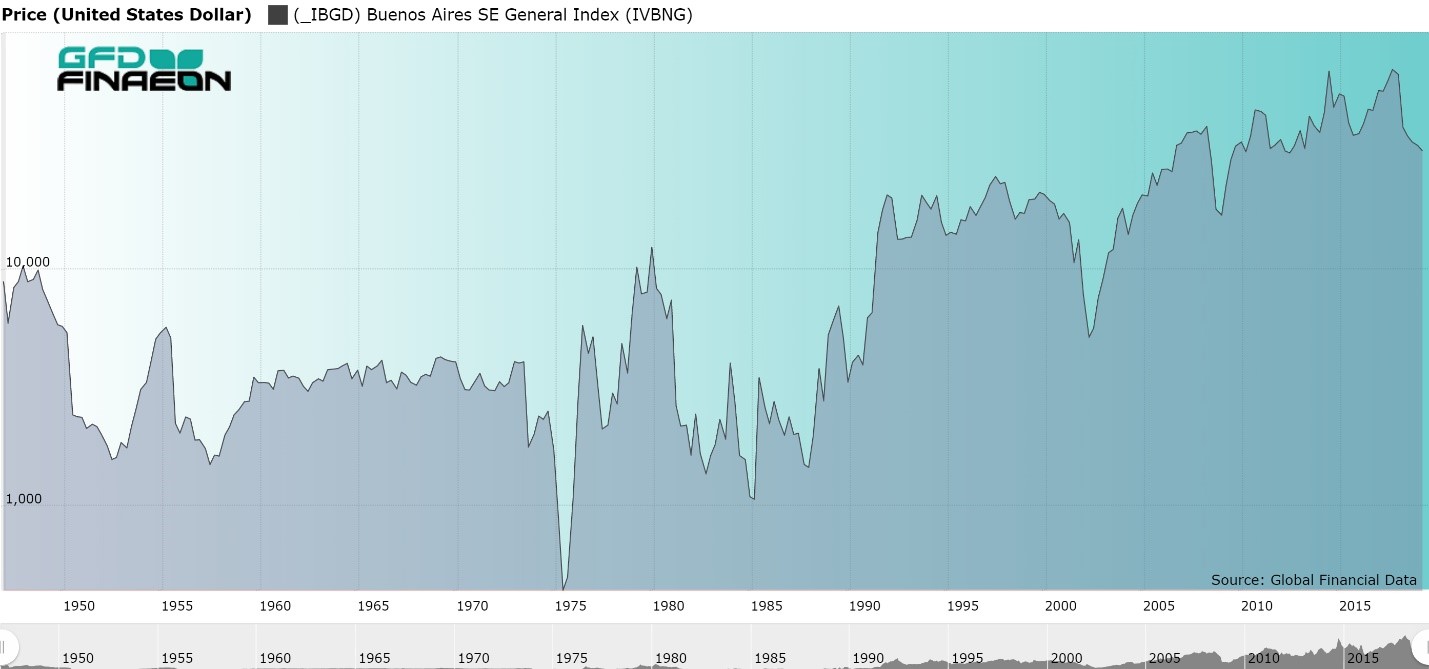

The instability in the Argentine stock market over the past 70 years is illustrated in Figure 2. The peso lost half of its value in 2018 and today (March 2019), MSCI’s stock market index, as measured in USD, is virtually the same level it was at in May 1992. Energy represents 40% of the stock market index and financials 17% with Tenaris SA, which manufactures steel pipes for energy companies representing 20% of the stock market’s capitalization and YPF representing 13.5%.

Bonds have suffered from Argentina’s instability as well. Between 1824 and 1953, Argentine bonds provided an annual return of 5.36%, but were made worthless by the inflation that destroyed the economy in the 1960s, 1970s, and 1980s. Since 1993, the EMBI index of government bonds returned 3.98% which is more than stocks which returned only 3.55% per annum between 1993 and 2018.

| Years | Price | Return | Inflation | Dividend | Real Return |

|---|---|---|---|---|---|

| 1865-1929 | 0.84 | 5.76 | 0.89 | 4.88 | 4.83 |

| 1929-1987 | 2.86 | 5.18 | 3.34 | 2.26 | 1.78 |

| 1987-1991 | 99.87 | 104.23 | 4.55 | 4.37 | 95.68 |

| 1991-2018 | 0.94 | 3.19 | 2.25 | 2.23 | 0.92 |

| 1929-2018 | 5.37 | 7.74 | 3.06 | 2.24 | 4.54 |

| 1865-2018 | 3.45 | 6.91 | 2.15 | 3.34 | 4.66 |

Table 1 allows us to compare returns in Argentina over long and short periods of time, converting all returns into U.S. Dollars. Over the past 153 years, Argentine stocks returned 4.66% per annum, after inflation. Returns were pretty much the same between Argentina’s period of stability (1865-1929) and instability (1929-2018).

The greatest contrast is between the returns during the four years of reform under Carlos Menem between 1987 and 1991 when investors received a real annual return of over 99% and returns since 1991. Investors received only 1.78% between 1929 and 1987 and the return to investors since 1991 has been only 0.92% per annum. Contrast this with annual returns after inflation of 6.66% in the United States since 1991.

What went wrong?

There was great anticipation that converting from the hyperinflationary Peso to the stable Dollar under President Menem would turn the economy around, but since 1991, investors have not shared the benefits of the growth they anticipated. Instead, the economy collapsed when Argentina was unable to maintain its link to the U.S. Dollar after 2001. The country has gone through a series of defaults and because Fernandez introduced capital controls, Argentina was downgraded from being an emerging market to being a frontier market. Macri has fought to return Argentina to a market-based economy that can attract more investment, but so far, this has not happened.

Argentina embodies the problems investors may face when they invest in emerging markets. There can be a few years of rapid growth when investors anticipate change, but also lost decades of slow growth when that change does not occur. Why would investors give up the relative stability of investing in the United States for the instability of investing in Argentina? Argentina is not committed to the market in the same way a developed country is. Argentina will face new elections in October 2019 and current polls show that Cristina Fernandez could defeat Macri and upend the changes he has introduced. As we all know from finance, the value of a company depends upon the present value of future cash flows, and future cash flows in Argentina are by no means guaranteed. Argentina has a record of political and economic instability which no one can ignore.

Argentina was able to sell a 100-year bond in June 2017, but a year later went to the IMF for a $56 billion loan. Argentina’s current inflation rate is 54%, and the peso has lost half of its value during the past year. Argentina embodies all of the risks that investors in emerging markets face. The willingness of investors to commit money to Argentina under Presidents Menem and Macri shows that investors are willing to invest when they see an opportunity. Unfortunately, Argentina also shows what can happen when a country does not follow through on its promises.

Most people know the basic story of the French Revolution. France’s aid to the United States indebted the nation leading to new taxes that fed a revolt against the king and the aristocracy. The Estates General was convened in May 1789, and on July 14, 1789, the Bastille was stormed marking the beginning of the French Revolution. The Declaration of the Rights of Man was passed and feudalism was abolished in August 1789. France became a republic in September 1792 and in January 1793, King Louis XVI was executed. A dictatorship gained power in 1793 under Robespierre and the Committee of Public Safety which introduced the Reign of Terror. In 1795, the Directory assumed control over France, suspended elections and repudiated debts. The Directory remained in power until 1799 when Napoleon Bonaparte overthrew the Directory in a coup and became the leader of France.

But what about investors? How were they affected by the French Revolution? The king lost his head, but investors lost their money.

Before the Revolution

Few people realize how active the Paris stock market was during the 1700s. The Paris stock exchange was founded on September 24, 1724, though shares in the French East India Co. (Compagnie des Indes) had traded in Paris for years. GFD has data on over 70 securities that traded on the Paris bourse in the 1700s. This includes 15 common stocks in 7 different companies, one corporate bond, 50 different government bonds and 6 issues of scrip, all faithfully recorded from issues of the Gazette de France. And this ignores the fact that Parisian investors were also able to invest in stocks and bonds in London and in Amsterdam during the 1700s.

It is interesting to note that French East India Co. stock suffered more volatility during the 1700s than shares in either London or Amsterdam. Compagnie des Indes shares rose over 4000% during the bubble in 1718 and 1719, only to lose 99% of their value during the crash that followed. There were five bull markets in which shares rose by over 90% in Paris in the 1700s and three bear markets in which shares fell by over 50%. The Paris stock exchange was not for the feint of heart. The rise and fall of Compagnie des Indes shares are illustrated in Figure 1.

The Paris stock exchange was formally closed on June 27, 1793 and all joint-stock companies were banned on August 24, 1793. But once the joint-stock companies were shut down, who would dispose of the assets of the companies? French East India Co. officials bribed government officials so the company, rather than the government, could oversee its liquidation, but once these bribes were uncovered, several of the company officials involved were arrested and later executed. The liquidation of the company produced only three ships which were liquidated in July 1795, and as a result, shareholders in the Compagnie des Indes lost virtually everything.

Bondholders met a similar fate. France defaulted on its pre-revolutionary debt in 1796, giving shareholders 1/3 the value of their old bonds in new 5% consolidated bonds which didn’t pay any interest until 1802. A similar loss occurred to Dutch shareholders, who also lost 2/3 of the value of their bonds. English bondholders suffered no default.

After the Revolution

Investors were decimated by the French Revolution. Bondholders lost 2/3 of the value of their bonds, and the French Revolution officially abolished joint-stock companies in 1793. Investors received very little compensation for their shares. Officials caught up in the bribery scandal in 1793 lost their lives. The Assignats, which were issued during the revolution, became almost worthless during the inflation that ravaged France. After inflation, 100 Francs in Assignats in 1789 were worth less than 5 centimes by 1796. More people were put to death for counterfeiting the eventually worthless Assignats than for any other crime committed during the French Revolution.

Just as the ancien regime collapsed during the French Revolution, so did the country’s finances. Investors were unable to sell their shares and bonds and fled to England where, at least, they wouldn’t lose their lives. As the Napoleonic Wars dragged on, other countries defaulted on their debts. The Swedes, Dutch, Portuguese, Spanish and Russians all suspended interest payments at some point during the Napoleonic Wars. Only English finances survived the Napoleonic wars intact.

After Napoleon gained power during a coup on November 9, 1799, he worked to rehabilitate France’s finances. Napoleon replaced the Livre Tournois with the French Franc. The 5% Consolidated Bonds were issued to replace outstanding French debt. Initially, the price of the bonds sank to 9.25 at the end of 1798, but once the government started paying interest, the price of the bonds recovered and the yield on the bonds fell as is illustrated in Figure 2. Napoleon established the Banque de France in 1801 to provide France with a central bank similar to the one that England had. The company’s shares became the largest joint-stock company on the bourse and traded in Paris until the bank was nationalized in 1946.

The re-establishment of France’s finances was a success. Between 1800 and 1914, Paris was the center of finance in continental Europe providing shareholders and bondholders during the 100 years before 1914 with one of the highest returns of any European country.

Investors and the French Revolution

Global Financial Data has collected centuries of data on interest rates. We wanted to highlight two data sets from the GFD Indices that cover government bond yields from 1285 to 2019 and that cover central bank deposit rates from 1522 until 2019. With these two charts, you can see how unusual the current decline in interest rates is, pushing yields down to levels that hadn’t been reached during the past seven centuries.

Government Bonds

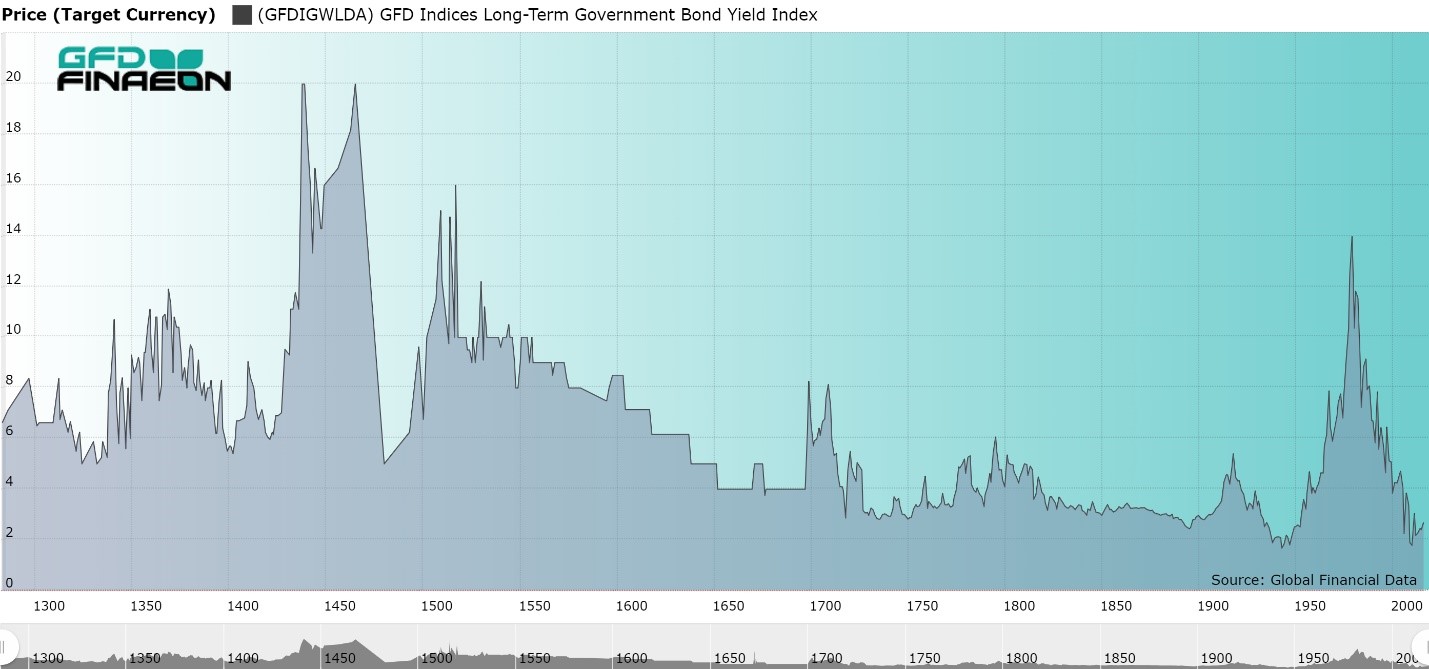

Figure 1 provides data on the yields on government bonds from 1285 until 2019. During the past 700 years, the financial center of the world has passed from Italy to the Netherlands to England to the United States. We have used data from each of these countries to create the graph provided below. Data includes the Prestiti of Venice from 1285 to 1303 and from 1408 to 1500, the Consolidated Bonds of Genoa from 1304 to 1408, the Juros of Spain from 1504 to 1518, Juros of Italy from 1520 to 1598, government bonds of the Netherlands from 1606 to 1699, English bonds, primarily the British Consol from 1700 to 1918 and United States 10-year bonds from 1918 to 2018.

Figure 1. Global Long-term Government Bond Yields, 1285 to 2018

The general trend in yields has been for rates to decline over the past 700 years, especially since 1550. Before then, yields often spiked when wars in Italy and elsewhere put the payment of interest and the redemption of the bonds at risk. Under normal circumstances, bonds would yield about 6%, but in two cases, failure to pay interest on outstanding bonds pushed yields up to almost 20% before the end of the wars eliminated the possibility of further default.

Since 1600, when Dutch bonds were substituted from Italian bonds, the risk of default has been virtually eliminated driving yields down from 6% in 1600 to close to zero today. In fact, many European and Japanese government bonds pay a negative yield. Since there is little risk of default, increases and decreases in yields have primarily been driven by inflation during the past three centuries, which explains both the rise in interest rates around World War I and between 1950 and 1980. As long as central banks can control inflation, government bond interest rates are likely to remain low for some time to come.

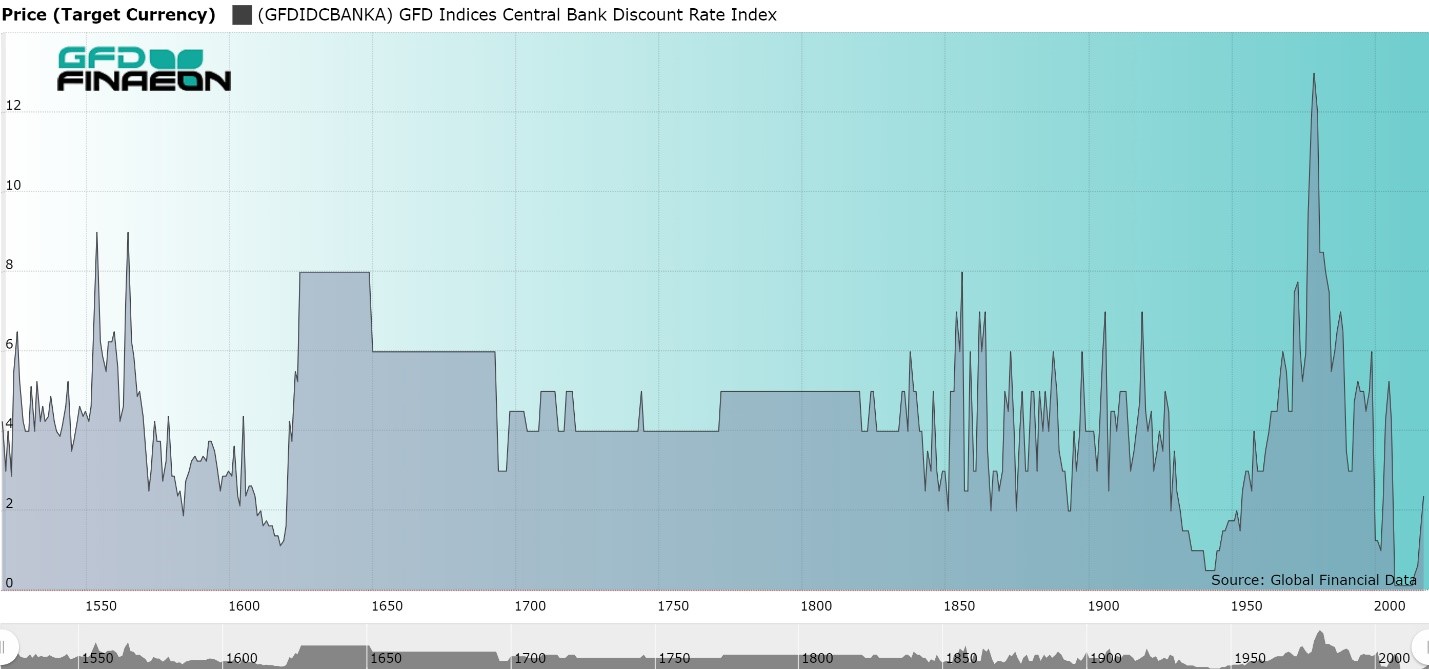

Central Bank Rates

Using treasury bills as a short-term alternative to cash began primarily during World War I. Consequently, treasury bills cannot be used to provide a long-term chart of interest rates; however, the interest rate central banks pay on deposits provide centuries of data.

Figure 2 provides a graph of interest rates over the past 500 years. The graph uses the deposit rate of the Bank of St. George in Genoa from 1522 to 1625, the legal limit on English loans from 1625 to 1692, the deposit rate for the Bank of England from 1693 to 1913, the Discount Rate of the Federal Reserve Bank of New York from 1913 to 2002 and the Federal Funds Target Rate since 2003.

Figure 2. Central Bank Deposit Rate, 1522 to 2018

As the graph shows, the deposit rate has fluctuated between 2% and 4% during the past 500 years. There were periods, such as the early 1600s, during World War II and during the past 10 years when interest rates fell below 2%, but these were exceptions to the rule. The highest short-term interest rates occurred in 1981 when inflation drove interest rates to double-digit levels for the first time in history. On the other hand, the Great Recession after 2008 drove interest rates to negative levels in Japan and Europe and almost to zero in the United States. These are truly unprecedented times.

Conclusion

This blog has provided over 700 years of history on bond yields and deposit rates in Europe and the United States. During the past seven centuries, the center of the financial world passed from Italy to the Netherlands to England and to the United States. We have used yields from each of these countries to put together these long-term charts. Both short-term and long-term yields today are driven by inflation rather than risk, and as long as inflation remains low, yields are likely to remain low for some time to come.

Global Financial Data has generated indices on the United States and the World Index excluding the United States since 1792. This enables us to compare the performance of stocks in the United States with the rest of the world over the past 225 years. Generally speaking, US stocks underperformed the rest of the world in the first half of the 1800s, but strongly outperformed the rest of the world since the Civil War. After a decline in the relative performance between 1967 and 1988, American stocks have generally outperformed the rest of the world over the past 30 years. Will this trend continue?

Figure 1. United States 100 Index Divided by GFD’s World x/USA Index, 1792 to 2018

During the civil war, the United States went off the gold standard and the U.S. Dollar declined in value relative to other currencies. This decline more than offset the inflation that occurred during the Civil War and the net effect was a further decline in U.S. stocks relative to the rest of the world. However, once the Civil War ended, U.S. stocks began a stead rise in value as the American economy industrialized. By the 1890s, Standard Oil was the largest company in the world. The rise in American stocks relative to the rest of the world was modest until 1896, but after that, American stocks began a steady rise in value relative to the rest of the world for the next 70 years.

Figure 1. United States 100 Index Divided by GFD’s World x/USA Index, 1792 to 2018

During the civil war, the United States went off the gold standard and the U.S. Dollar declined in value relative to other currencies. This decline more than offset the inflation that occurred during the Civil War and the net effect was a further decline in U.S. stocks relative to the rest of the world. However, once the Civil War ended, U.S. stocks began a stead rise in value as the American economy industrialized. By the 1890s, Standard Oil was the largest company in the world. The rise in American stocks relative to the rest of the world was modest until 1896, but after that, American stocks began a steady rise in value relative to the rest of the world for the next 70 years.

Figure 2. USA-100 and World x/USA Price Indices, 1864 to 2018

Table 1 provides a comparison of the returns during different periods of time to stocks in Europe, the World x/USA and to the United States. During the three eras, the United States underperformed the rest of the world only during the Free Trade Era, and most of this occurred before the civil war when finance firms dominated the American market. However, since 1864, American stocks have outperformed the rest of the world and European stocks in every era.

Figure 2. USA-100 and World x/USA Price Indices, 1864 to 2018

Table 1 provides a comparison of the returns during different periods of time to stocks in Europe, the World x/USA and to the United States. During the three eras, the United States underperformed the rest of the world only during the Free Trade Era, and most of this occurred before the civil war when finance firms dominated the American market. However, since 1864, American stocks have outperformed the rest of the world and European stocks in every era.

Table 1. Price Index Annual Returns to Europe, World x/USA and USA-100

If you look at total returns including dividends, you get similar results.

Table 2. Return Index Annual Returns to Europe, World x/USA and USA-100

The peak in the relative outperformance of U.S. to the rest of the world occurred in 1967, but during the next 20 years, between an underperforming stock market and a decline in the value of the Dollar, U.S. stocks fell back to the level they had been at before Pearl Harbor. The decline in the relative performance of U.S. Stocks was also driven by the Japanese bubble of the 1980s. It should be remembered that in 1989, the capitalization of the Japanese stock market was larger than that of the United States. Today, the capitalization of the Japanese stock market is less than 20% of the American stock market.

Figure 3 compares the U.S. market to Europe since 1900. The relative decline in U.S. stocks relative to Europe in the 1980s was not as sharp as the World excluding the United States index. Figures 1 and Figure 3 are very similar up until the 1960s, but the two of them diverge in the 1980s. The U.S./Europe graph declined back to the level it has been at in the 1920s, and reached a lower low in 2008 when the Financial Crisis drove the U.S. stock market down to new lows. Since then, however, U.S. Stocks have risen to new highs relative to Europe.

Figure 3. American stocks relative to European Stocks, 1900 to 2018

Since 1988, the United States has outperformed the rest of the world as globalization, computers, and biotechnology have driven the American market forward. It should have been obvious that the U.S. stock market was undervalued relative to the rest of the world at the bottom of the financial crisis in 2008. Now both graphs are at peaks relative to the past with the U.S./European graph reaching new highs. The question is whether the U.S. market will run out of steam and reverse relative to the rest of the world, or continue its steady increase in value.

Figure 3. American stocks relative to European Stocks, 1900 to 2018

Since 1988, the United States has outperformed the rest of the world as globalization, computers, and biotechnology have driven the American market forward. It should have been obvious that the U.S. stock market was undervalued relative to the rest of the world at the bottom of the financial crisis in 2008. Now both graphs are at peaks relative to the past with the U.S./European graph reaching new highs. The question is whether the U.S. market will run out of steam and reverse relative to the rest of the world, or continue its steady increase in value.

US and the World in the 1800s

Figure 1 shows the relative performance of GFD’s US-100 index and GFD’s World x/USA index between 1792 and 2018. Between 1792 and 1864, American stocks underperformed the rest of the world. There were two reasons for this. Until the 1830s, the U.S. stock market included finance stocks almost exclusively. Banks could not operate across state lines and many of the banks could only operate from one location. Thus, the opportunities for growth were limited. If you include the dividends American banks paid, they provided a positive return of 4% per annum before the Civil War, but on average, the price of stocks declined in the United States between 1792 and 1860 by about 1% per annum. In Europe, on the other hand, increases in the share price of canals and railroads supplemented the growth of central banks, providing positive, if modest returns.

Figure 1. United States 100 Index Divided by GFD’s World x/USA Index, 1792 to 2018

During the civil war, the United States went off the gold standard and the U.S. Dollar declined in value relative to other currencies. This decline more than offset the inflation that occurred during the Civil War and the net effect was a further decline in U.S. stocks relative to the rest of the world. However, once the Civil War ended, U.S. stocks began a stead rise in value as the American economy industrialized. By the 1890s, Standard Oil was the largest company in the world. The rise in American stocks relative to the rest of the world was modest until 1896, but after that, American stocks began a steady rise in value relative to the rest of the world for the next 70 years.

The United States Outperforms the Rest of the World

The United States suffered from neither the destruction of World War I and World War II nor the economic chaos, inflation and nationalizations that plagued Europe in the first half of the 1900s. Between 1914 and 1929, American stocks rose rapidly in price relative to the rest of the world. U.S. stocks fell back during the Great Depression of the 1930s and hit another low point in 1941, right before Pearl Harbor was attacked, but the next 25 years showed steady growth of U.S. stocks relative to the rest of the world. Almost all of this advance happened in the 1940s as Europe was devastated by World War II. However, even as Europe recovered from the war, American stocks continued to outperform the rest of the world until 1967. Figure 2 compares the performance of the US-100 and the World x/USA index between 1864 and 2018.

Figure 2. USA-100 and World x/USA Price Indices, 1864 to 2018

Table 1 provides a comparison of the returns during different periods of time to stocks in Europe, the World x/USA and to the United States. During the three eras, the United States underperformed the rest of the world only during the Free Trade Era, and most of this occurred before the civil war when finance firms dominated the American market. However, since 1864, American stocks have outperformed the rest of the world and European stocks in every era.

| Period | Years | Europe | World x/USA | USA |

|---|---|---|---|---|

| Free Trade | 1799-1914 | 1.58% | 1.80% | 0.91% |

| Regulation | 1914-1981 | 1.93% | 2.65% | 4.38% |

| Globalization | 1981-2018 | 7.15% | 6.27% | 8.25% |

| Post-WWI | 1914-2018 | 3.74% | 3.91% | 5.73% |

| Post-Civil War | 1864-2018 | 2.67% | 2.79% | 4.63% |

| All | 1792-2018 | 2.44% | 2.64% | 2.96% |

| Period | Years | Europe | World x/USA | USA |

|---|---|---|---|---|

| Free Trade | 1799-1914 | 5.30% | 5.58% | 7.10% |

| Regulation | 1914-1981 | 6.00% | 6.79% | 0.98% |

| Globalization | 1981-2018 | 10.56% | 8.95% | 11.13% |

| Post-Civil War | 1864-2018 | 5.98% | 5.98% | 9.13% |

| Post-WWI | 1914-2018 | 7.59% | 7.55% | 2.71% |

| All | 1792-2018 | 6.28% | 6.40% | 8.20% |

Figure 3. American stocks relative to European Stocks, 1900 to 2018

Since 1988, the United States has outperformed the rest of the world as globalization, computers, and biotechnology have driven the American market forward. It should have been obvious that the U.S. stock market was undervalued relative to the rest of the world at the bottom of the financial crisis in 2008. Now both graphs are at peaks relative to the past with the U.S./European graph reaching new highs. The question is whether the U.S. market will run out of steam and reverse relative to the rest of the world, or continue its steady increase in value.