We are about half way through January and many analysts, investors and market enthusiasts are wondering which way that markets are headed. Typically, the markets go through the “January Effect” which is a general increase in stock prices during the month of January. This rally is generally attributed to an increase in buying, which follows the drop in price that typically happens in December when investors, seeking to create tax losses to offset capital gains, prompt a sell-off. For 2014, this move has been less evident, as a matter of fact, the markets have been flat for the US and Europe (expect Greece) where as Asia has been down. What is going this January? Could it be that many investors are re-balancing their portfolios by selling part of their profits from 2013 in stock and re-allocating the proceeds to bonds? January is a common time for re-balancing and tax harvesting. The S&P 500 gave us about 30% returns in 2013 and profit taking is common to lock in some of those gains. Will 2014 bring us similar returns to 2013?

We are about half way through January and many analysts, investors and market enthusiasts are wondering which way that markets are headed. Typically, the markets go through the “January Effect” which is a general increase in stock prices during the month of January. This rally is generally attributed to an increase in buying, which follows the drop in price that typically happens in December when investors, seeking to create tax losses to offset capital gains, prompt a sell-off. For 2014, this move has been less evident, as a matter of fact, the markets have been flat for the US and Europe (expect Greece) where as Asia has been down. What is going this January? Could it be that many investors are re-balancing their portfolios by selling part of their profits from 2013 in stock and re-allocating the proceeds to bonds? January is a common time for re-balancing and tax harvesting. The S&P 500 gave us about 30% returns in 2013 and profit taking is common to lock in some of those gains. Will 2014 bring us similar returns to 2013?

The new US $100 bill is out, as you may have seen this holiday season. Our dear old Uncle Ben is a technological wonder with a dozen different anti-counterfeiting devices on it. Since there are more $100 bills circulating outside of the United States than inside, the U.S. Government has to insure that counterfeiters are unable to replicate the government’s most treasured export. This raises the question, who was the greatest counterfeiter of all time?

The new US $100 bill is out, as you may have seen this holiday season. Our dear old Uncle Ben is a technological wonder with a dozen different anti-counterfeiting devices on it. Since there are more $100 bills circulating outside of the United States than inside, the U.S. Government has to insure that counterfeiters are unable to replicate the government’s most treasured export. This raises the question, who was the greatest counterfeiter of all time?

Government Counterfeiting

- The Roman Empire replacing its silver Denarii with billon Antonininii;

- The Khans of China creating the first paper inflation in the 1300s;

- The United States making its first currency, the Continental Dollar, worthless;

- Germany hyperinflating out of its debts by creating trillions of marks;

- Or the US Federal Reserve blowing up its balance sheet.

- Barbarians did of the Roman gold Aureus

- British did of Continental Dollars and French Assignats during the 1700s

- Germans did of British Pounds during World War II in Operation Bernhard

- United States did of Japan’s Occupation currency of the Philippines

- North Koreans did of US Dollars, making them one of their principle exports.

A Classy Counterfeiter

Our vote for the greatest counterfeiter of all time goes to Artur Alves dos Reis whose story was recounted by Murray Teigh Bloom in The Man Who Stole Portugal. Reis was both smart and classy, and his criminal operation reflected these qualities. To my knowledge, Reis put together the most audacious counterfeiting scheme in history. He conceived his master plan while he was in jail in Oporto for embezzling the funds of a company he had taken over. Some criminals sit in jail and try to avoid repeating their misfortunes. Others, like Reis or Tony de Angelis, think-up bigger, more foolproof schemes. While he was sitting in his cell, Reis put together his master plan that would make him the richest, and possibly the most influential man in Portugal in only one year.Although you may not realize it, counterfeiting is a very complex operation. To be successful, (i.e. not get caught), be able to spend your money, and not receive free room and board from the government, you have to do three things successfully. First, you have to create counterfeit currency that can’t be detected. Second, you need a way of laundering the money and converting it into real assets so you can enjoy the fruits of your ill-begotten labors. Third, you must make sure that you avoid the triple curse of detection, arrest and conviction. Let’s see what Reis’s solution was to this age-old problem.Step One: Create an Undetectable Banknote

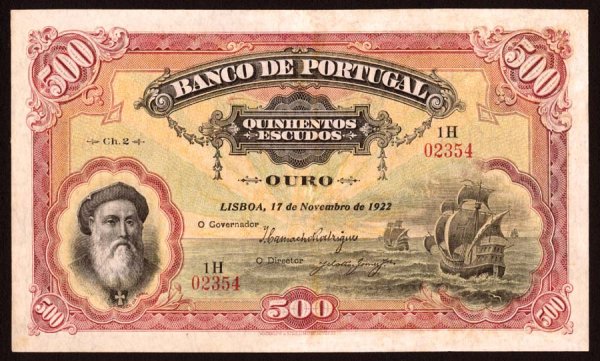

First, create a counterfeit that can’t be detected. During the 1920s, the Banco do Portugal had the exclusive right to print currency in Portugal. The bank used foreign printing companies with superior anti-counterfeiting technology to protect their banknotes. The English company, Waterlow & Sons, printed the 500 and 1000 Escudo notes (equal to about $25 and $50 in 1923) for the Banco do Portugal. So why not get Waterlow & Sons to print the notes for Reis as well?Reis was a natural-born forger. He forged his diploma as an engineer from Oxford as a “joke”, but this helped land him a job as a government railroad inspector in Angola at the age of twenty-two. In 1924, he forged $100,000 worth of checks and used the money to take over control of Ambaca, the Royal Trans-African railway Company of Angola. He then used the money in the company’s treasury to cover his own checks. He was arrested in July 1924 for embezzlement, but was released two months later when a court decided his was a civil and not a criminal case. It was during the two months he was the guest of the Oporto police that he conceived his infamous counterfeiting scheme. The key was to find someone with a respected name who could help him convince Waterlow & Sons to print banknotes secretly for Reis. He found three men of questionable repute, but with connections to help Reis: Jose Bandeira, Gustav Adolf Hennies and Karel Marang. Bandeira got his brother, the Portuguese Minister to the Netherlands, to give Marang a letter introducing him as a respected Dutch citizen who had a power-of-attorney for Alves Reis to negotiate the printing of the banknotes. Marang went to Waterlow & Sons in London, and presented his letter of introduction as the “Consul General of Persia” on forged Banco do Portugal stationary to Sir William Waterlow. Marang spun the story Reis had instructed him to give. A private syndicate was being formed to save the colony of Angola from its current dire financial condition with a $5,000,000 investment. In return for the loan, the syndicate would be allowed to print and circulate banknotes in Angola. Waterlow & Sons would print the banknotes for the syndicate, and once the notes reached Angola, the banknotes would be supercharged with the word ANGOLA so they wouldn’t be confused with notes from the mother country. The whole affair had to be kept secret lest Angola fall into further financial difficulties due to ill-placed rumors of pending economic ruin. Of course, Sir William knew that supercharging notes was normal practice for Portugal’s colonies, and that the Banco Ultramarino had the exclusive right to print banknotes for the Portuguese colonies. This was an opportunity for Waterlow & Sons to get this business away from Bradbury, Wilkinson & Co., the current printer of banknotes for the Banco Ultramarino in Angola. Marang asked Waterlow to print the 500 Escudo note with Vasco da Gama on it. The deal was signed on January 6, 1925, and for the printing cost of $7,200, Reis and his conspirators would receive $5,000,000 in banknotes, a 70,000 percent return on their investment. Bandeira picked up the first group of notes from Waterlow & Sons on February 10, and by March 20, they had 100 million Escudos ($5,000,000) in Portuguese banknotes. Bandeira used his orange diplomatic card to transport the bills in luggage marked the “Legation of Portugal” across the borders without detection. After the first step had been successfully completed, they placed an order for an additional 190 million Escudos in banknotes ($9,500,000). Of course, the banknotes never made it to Angola.

The greatest risk in the scheme was having banknotes with duplicate numbers discovered, but this was the lesser of two evils. If Reis and Marang had requested banknotes outside the numerical range of the 500 Escudo notes, the spurious notes would have been quickly discovered. The lower risk lay in duplicating the existing serial numbers, and hoping the counterfeiters were able to successfully release all the banknotes before the law of large numbers caught up with them.

Step Two: Laundering Money with Your Own Bank

Step One of the plan was complete, now for Step Two: laundering the money. A small-scale counterfeiter can pass bills through petty criminals, but the notes Reis and friends had were equal to almost 1% of Portugal’s GDP. This was the equivalent of over $150 billion if the same amount had been released in the United States today. Even if Reis hired every petty criminal in Lisbon and Oporto, he wouldn’t be able to unload a fraction of the banknotes.

Step Three: Avoid Detection (For a While)

Step Three and the most important of all was how to avoid detection, arrest and imprisonment. For this, Reis had a brilliant solution. Since they were counterfeiting Banco do Portugal banknotes, only the Bank could initiate proceedings to prosecute them. But what if –just what if– Reis controlled the shares in the Banco do Portugal? The bank had already exceeded its statutory banknote limit many times over and the directors of the Banco do Portugal had never been prosecuted, so why should they prosecute Reis? Or as Reis put it, “How can they arrest us when they’re us and we’re them?”Like most European countries, Portugal had suffered inflation after World War I. Prices had increased 48% per annum between 1919 and 1924, and the Escudo had depreciated by 87% against the Pound Sterling. Although the Banco do Portugal was only supposed to issue banknotes thrice its capital, it had, in fact, issued banknotes a hundred times its capital. By comparison with this, Reis’s monetary manipulations were minor by comparison. The chart below shows the depreciation of the Portuguese Escudo against the U.S. Dollar after World War I.

The Scam Exposed

The crisis broke on December 4, 1925 when the newspaper O Sêculo published an expose of the Banco Angola e Metropole. When one of its branches was closed, huge caches of duplicate 500 Escudo banknotes were discovered. Reis, his compatriots, and almost anyone associated with the Banco Angola e Metropole, (save Hennies who had sailed on), were arrested. Incredibly enough, the Governor and the Vice Governor of the Banco do Portugal were also arrested, so convincing were Reis’s forged documents. It was as if Ben Bernanke and Janet Yellen had been arrested for counterfeiting!The Banco do Portugal faced a tough decision. What should it do with all the 500 Escudo notes? It was impossible to differentiate between the original and the duplicate banknotes because they were printed by the same printer using the same plates. The Banco do Portugal came to the only conclusion possible. Every single Vasco da Gama 500 Escudo note would have to be withdrawn from circulation. People could exchange up to 200 of the Vasco da Gamas for 1000 Escudo notes until December 26. After that, they would be worthless. The revelation of the counterfeiting plot created a huge loss of confidence in the corrupt, democratic government. Military officers who were aggrieved over their pay failing to keep up with inflation, overthrew the democratic government on May 28, 1926. This eventually led to the dictatorship of Portugal by Dr. Antonio de Oliveira Salazar (who had been Portugal’s Finance Minister) in 1932. Salazar remained dictator of Portugal until his death in 1968. A scheme to counterfeit currency and make a forger rich had led, indirectly, to the downfall of a democracy which was followed by a forty-year dictatorship. Reis remained in jail and was found guilty on June 29, 1930 of falsely introducing 330,000 banknotes into Portugal. He was sentenced to twenty years in prison. His compatriots were found guilty as well, but received lesser sentences. Reis was released from prison on May 14, 1945, and died ten years later. Sir William Waterlow was sued by the Banco do Portugal for damages for printing the banknotes. Of course, Waterlow had no knowledge of the counterfeiting scheme and as his lawyers argued, no actual damage had been done to the bank by the banknotes. If anything, Portugal was better off as a result of Reis’s unconventional stimulus plan. Though Waterlow spent a million dollars on lawyers defending him, he lost the case and Waterlow & Sons was forced to pay of £610,392 (about $3,000,000) in damages. There must be a certain irony in the fact that as a result of the lawsuit, the main beneficiary of the scheme to counterfeit the banknotes was the Banco do Portugal itself. Sir William died of peritonitis in 1931 and the case was settled in April 1932. Reis was the last of the great counterfeiters. His scheme had style and panache, as did he. His story ripped through the papers just as his scam ripped through the economy. This case study should not be forgotten nor should we forget Reis and the ingenuity that rested behind his schemes. The piranha of Portugal may be gone, but there will always be a new Wolf on Wall Street attempting to profit at the expense of others. When most people think of Venice, they think of the visuals of Venice: the canals, the gondoliers, the paintings by famous artists such as Canaletto or Titian, the Bienniale, or St Mark’s Square (named after the saint whose relics the Venetians stole from Alexandria in 828 by hiding them beneath pork to get them past the Muslim inspectors) and its pestering pigeons.

When most people think of Venice, they think of the visuals of Venice: the canals, the gondoliers, the paintings by famous artists such as Canaletto or Titian, the Bienniale, or St Mark’s Square (named after the saint whose relics the Venetians stole from Alexandria in 828 by hiding them beneath pork to get them past the Muslim inspectors) and its pestering pigeons.

BIRDS, BOATS AND BONDS

PRESTITI: THE FIRST AAA EUROBONDS

Venice was the first country to issue government bonds to its citizens in the same way governments currently issue government bonds. Before the Venetian prestiti, and even after, kings, queens, emperors and others borrowed money to fight wars or feed their royal megalomania. When the rulers were unable to pay back the loans, they simply defaulted, often bankrupting their creditors. Venice was different. Venice was the medieval equivalent of Athens, a democracy for the elites. In 726, the Venetians rebelled against their Roman/Byzantine rulers over the Iconoclast controversy and elected the first of 117 doges before Napoleon conquered the city in 1797. Venice became a city-state, expanding its commercial reach, and became an imperial power, eventually capturing and sacking Constantinople in 1204 during the Fourth Crusade. By the late thirteenth century, Venice was the most prosperous city in all of Europe. At the peak of its power and wealth, it had 36,000 sailors operating 3,300 ships, dominating Mediterranean commerce. Defending their empire meant wars with other Italian city-states, such as Florence and Genoa, and wars meant borrowing money.THE PRICE OF PRIZED PERPETUITIES

Venice introduced the prestiti in the twelfth century. Subscriptions were obligatory on wealthy citizens in proportion to their wealth, and the elites of Venice found forced loans preferable to outright taxation. In 1262, Venice lost control over Constantinople, and the outstanding loans, which had been considered temporary, were consolidated into one permanent fund called the monte vecchio. This move institutionalized the prestiti as long-term loans rather than short-term borrowings. The prestiti paid a nominal interest rate of 5% on the outstanding capital, two installments of 2.5% paid per annum. After 1377, interest rates were variable, and rates were reduced to 4% in the 1400s. In 1482 a new series of prestiti, the monte nuovo, was issued based upon a new kind of tax and the interest rate was restored to 5%. Another new series, the monte novissimo, was issued in 1509 during the war with the League of Cabrai, and finally the monte sussidio was introduced in 1526. The prestiti were perpetuities that had no specific maturity date. No physical bonds were issued, but all bonds were registered through the Loan Officers, the Ufficiali degli Prestiti. The claims on these bonds could be sold and transferred to others who then had all the rights of the original purchasers. When possible, the Venetian government repaid the principal. The prestiti became popular forms of investment for Venetian nobles. They were used as endowments for charities, and were used as dowries for daughters upon their marriage. Since the elites of Venice owned prestiti and were part of the government, this reduced the likelihood the city would default on its debts (though the government did forgo interest payments in 1379-1381, 1463-1479 and 1480). Owning prestiti was a privilege. Foreigners, who trusted the Venetian government more than their own, could only obtain prestiti through an act of the Council of Venice. The prestiti were fully paid off by the government of Venice in the late 1500s. As with any bond, as the price of the prestiti went down, the yield went up. During a war, the price of prestiti would fall as new bonds were issued and owners faced the risk of delays in payment of principal and interest. During peace time, the price rose as the risk diminished. Since the price of trades in prestiti was a matter of public record, potential purchasers could use these prices to determine the riskiness of their investment. Thus, the prestiti became a barometer of the Venetian Republic. When there was peace, the government would repay outstanding prestiti, sometimes by issuing new prestiti, rolling over old loans into new, but when Venice was at war, the government would issue new prestiti. The prestiti were exempt until 1378 from assessment of new forced loans if held by the original owner, and new assessments were levied largely on real estate. Venice was successful with the issue of prestiti because the right to transfer the bonds through the Ufficiali degli Prestiti made the bonds liquid and fungible. The Venetian government established a long record of regular payment of interest even when war and disaster threatened the state, assuring investors that they would not lose their money from a royal default. As Venice prospered, confidence in payments rose. The government was under a legal obligation to pay the prestiti, and payment was not left to the whim of the king. During peace time, extra revenues were directed to repayment of the prestiti, rather than setting aside money for the Venetian war chest or expanding services. The government had a deliberate policy of repurchasing prestiti whenever their price fell. In short, the prestiti were the AAA bonds of their day, and as Venice prospered, so did the city and its bondholders.THE VAGARIES OF WAR IMPACT THE PRESTITI

As all nations know, wars do not always go as planned. Sidney Homer, in his History of Interest Rates, provides historical data on the prices of prestiti, and you can see how the price of the bonds and their yield fluctuate in response to the fortunes of Venice. When Venice imposed large assessments, as in 1311-1314, the price of the prestiti fell, and when Venice made large repayments, as in 1344, the price could exceed 100. The worst decline in the fourteenth century came during the War of Chioggia between 1378 and 1381 with Genoa, during which Venice imposed very large assessments, suspended interest payments, made the prestiti no longer immune from tax levies, and expanded the debt 6 to 9 times its level in 1344. The price sank as low as 19 as a result. After the War of Chioggia ended, the prestiti fought their way back as confidence in the Venetian government returned, causing the price to rise to the 60 level. Unfortunately, the fifteenth century was one of ongoing wars in the Mediterranean. Venetian wars with Hungary in 1412, the Turks in 1416, Milan during the 1420s, and wars with both Florence and Milan in 1450 and the costs associated with these wars reduced confidence in the Venetian government’s ability to fund the prestiti. Emboldened by the fall of Constantinople in 1453, Sultan Mehmet II declared war on Venice, leading to a disastrous and protracted conflict between 1464 and 1479 which drove the price of prestiti back to the 20s. This led to the reissue of new prestiti as monte nuova in 1482. The graph below shows the yield on the prestiti from 1285 to 1502, assuming a 5% coupon (though in reality the prestiti paid a variable rate after 1377 and 4% during part of the 1400s). The impact of the War of the Chioggia in the 1370s and the wars with Milan and the Turks after 1420 are clearly seen. As the Venetian Republic’s empire shrank, holders of the prestiti suffered. Venetian bonds would definitely have been downgraded as the heavy impact of the Venetian wars had their effect on the city-state’s finances.

Venice never recovered from the devastating war with the Turks, not only because of the loss of its colonies in the Mediterranean, but because Portugal’s discovery of a sea route to India and Christopher Columbus’s discovery of America shifted the locus of economic power from the Mediterranean to the Atlantic. The ocean-faring sailing ships of France, England and the Dutch Republic replaced Venice’s oared galleys. Amsterdam replaced Venice as the financial center of Europe, and during the 1600s and 1700s the East India Company dominated the oceans around Asia the way Venice had dominated the Mediterranean until then. On May 12, 1797, Napoleon Bonaparte brought an end to the Venetian Republic.

Would you have liked to have invested in the greatest invention of all time? A machine that almost revolutionized the world and could have provided cheap, efficient energy to mankind for centuries to come! Then John Keely had the machine for you. Once perfected, the “hydro-pneumatic pulsating vacuo-motor engine” would have been used by every person in the world and would have made you rich. If you wanted to profit from the opportunity of a lifetime, then you should have invested in the Keely Motor Company. Unfortunately, the company no longer exists since Keely died in 1898. While Keely managed to make himself a rich man, his investors did not share the same fate. Nonetheless, the story of his perpetual motion machine will surely fascinate you.

Would you have liked to have invested in the greatest invention of all time? A machine that almost revolutionized the world and could have provided cheap, efficient energy to mankind for centuries to come! Then John Keely had the machine for you. Once perfected, the “hydro-pneumatic pulsating vacuo-motor engine” would have been used by every person in the world and would have made you rich. If you wanted to profit from the opportunity of a lifetime, then you should have invested in the Keely Motor Company. Unfortunately, the company no longer exists since Keely died in 1898. While Keely managed to make himself a rich man, his investors did not share the same fate. Nonetheless, the story of his perpetual motion machine will surely fascinate you.

H2O EXTRACTS GAS AND ATTRACTS MONEY

Born in Philadelphia on September 3, 1837, John Ernst Worrell Keely worked various jobs as a young man, as a member of a theatrical orchestra, a painter, a carpenter, a carnival barker, and as a mechanic. Then in 1872, he announced the discovery of a machine that could revolutionize the world. He said he had discovered a new physical force that could produce phenomenal power, never before heard of. Keely proposed to use the power of atoms in water to create perpetual motion. Since water covers more of the earth than land, the fuel for his machine would be cheap and readily available for all of mankind to benefit from. Keely’s basic idea, as he explained it to his awed listeners, was that atoms were in constant vibration, so all you had to do was to harness and channel the random vibrations of the atoms within water and you could produce unlimited energy. If you could get atoms to vibrate in unison, you could use their “etheric force” to run any motor of any size. To promote his discovery, Keely went on a speaking tour to share his great discovery with the world. At each engagement, someone in the audience would ask “How did you come to this great discovery?” Keely would explain to the audience that the revelation had hit him while he was playing a few notes on the violin. The notes on the instrument had set in motion harmonic vibrations, and in a moment of serendipitous inspiration, he had realized that the vibrations of atoms could be used to create energy just as the vibration of notes could be used to create music that could soothe the beast. Keely’s next stop was New York where he invited potential investors to the plush hotel he was staying at on Fifth Avenue. There, in his expansive suite with velvet chairs, chandeliers and extravagant mirrors, Keely explained his invention to potential investors while serving them delicacies to eat and liquor and champagne to savor and imbibe. Bankers, businessmen, engineers, lawyers, and other rich investors went to the hotel to invest in the sensation of the century. Soon after, with his first investment of $1 million in hand, he formed the Keely Motor Company. The corporation quickly grew to $5 million in capitalization. His investors wondered why the name of John Ernst Worrell Keely shouldn’t stand alongside that of Thomas Alva Edison and Alexander Graham Bell in the pantheon of great American inventors.ETHERIC DISINTERGRATION

Keely impressed potential investors with phrases such as “quadruple negative harmonics,” “etheric disintegration,” and “atomic triplets” when he revealed his ideas to eager listeners. Through the “liberator” which was a system of highly sensitive tuning forces, Keely would unleash the secret powers of the universe through his “hydro-pneumatic, pulsating vacuum energy” to solve the world’s energy problems forever. Keely demonstrated his machine to his guests, using his powers of prestidigitation to pour water into his vacuum engine and demonstrate his device. After a little bit, the engine gurgled, then rumbled, then came alive, providing a pressure of 50,000 psi to the amazed onlookers. As The New York Times wrote on June 11, 1875, the “generator” was reported to be about 3 feet in size, made of Austrian gunmetal in one piece, and held about ten or twelve gallons of water. Its inside was made up of cylindrical chambers connected by pipes and fitted with stopcocks and valves. The “receiver” or “reservoir” was about forty inches long by six inches in diameter and connected to the “generator” by a one inch diameter pipe. Keely claimed that his apparatus would generate his “vapor” from water solely by mechanical means without using any chemicals and claimed that it could produce 2,000 psi in five seconds. Whenever Keely demonstrated one of his machines, he would provide an elaborate explanation of how the engine worked, as illustrated by one of Keely’s exercises in eloquent embellishment from The New York Times on June 7, 1885: “It is an elaboration of interatomic ether by vibration. The atomic ether vibrates all around the molecules of matter. There is a magnetic force attached to it at the same time, and it assimilates with the molecular atomic aggregations – that is, assimilates with a certain attractive force that it is hard to tell what it is. I call it a vibratory negative. It doesn’t act like a magnet drawing metals toward it. There is a certain magnetic effect about it that causes it to adhere by vibratory rotation to different forms of matter – that is the molecular, atomic, etheric, and ether-etheric. The impulse is given by metallic impulses, the rotary power that is formed by etheric vibration – that is the force that holds it in position.” Even if you didn’t understand Keely’s theories, he had demonstrated to potential investors that his machine actually worked. What else mattered?A VIBRATING DEMONSTRATION

On November 10, 1874, Keely demonstrated the first full-scale version of his miracle machine at his laboratory at 1422 North Twentieth Street in Philadelphia, which he called the “etheric generator,” later to be called a “vibratory-generator.” The motor obtained its power from “intermolecular vibrations of ether” which allowed him to create a machine which he finally named the “hydro-pneumatic pulsating vacuo-motor engine.” The press simply called it a perpetual motion machine, though Keely never referred to it as such.

Investors and shareholders happily took the long trek to his factory in Philadelphia where he gladly demonstrated the current version of his hydro-pneumatic pulsating vacuo-motor engine to visitors. One spectator at a Keely demonstration described the power of the machine. “Great ropes were torn apart, iron bars broken in two or twisted out of shape, bullets discharged through twelve inch planks, by a force which could not be determined.” Keely often used a harmonica, violin, flute, zither or pitch pipe to activate his machines.

CONDUCTOR OF MUSIC, ELECTRICITY, AND STOCK

One of Keely’s biggest supporters was a widow by the name of Mrs. Clara Jessup Bloomfield-Moore, who not only invested $100,000 in the Keely Motor Co., but provided Keely with $2000 a month for personal expenses. When others began to lose faith in Keely because of the inevitable delays, Clara would invest more money and urge others to do the same. Ms. Bloomfield-Moore even wrote articles for prominent magazines of the day, praising Keely and his invention, saying that Keely’s etheric force was “like the sun behind the clouds, the source of all light though itself unseen. It is the latent basis of all human knowledge…” Whenever there were doubts that his engine would finally come to fruition, Keely would unveil his newest advancement in tapping the forces of nature. At one demonstration, he showed investors the “shifting resonator” which carried seven different kinds of vibration, each “being capable of infinitesimal division.” Keely would set the whole contraption going in a variety of ways; sometimes by playing a few notes on his violin, a zither, a harmonica, or even an ordinary tuning fork. Whatever the method, etheric force came forth, starting the motor and impressing the investors. The stock went public on the New York Stock Exchange in January 1890, the greatest place for venture capital in the United States. The stock traded steadily during the 1890s, neither shooting up in a bubble nor collapsing. With no profits and no dividends, there was no reason for the stock to skyrocket until the etheric vibrations were turned into a money-making machine for the company’s shareholders.

Unfortunately, there were scientists who were skeptical of Keely’s claims. In 1884, the Scientific American ran an article stating that everything Keely had done could be replicated using compressed air. Was some hidden source of compressed air the secret of Keely’s wonder machine and not the etheric force he theorized about? Keely dismissed these “scientists” as petty and envious men. Hadn’t others scoffed at the steamship, the telephone, the telegraph and the electric light? When Mrs. Bloomfield-Moore suggested that he share his secrets with Thomas Edison and Nikola Tesla to improve the prestige of the company, Keely refused to tell anyone about his creation. He didn’t need others to validate his invention, he asserted.

DISINTERGRATION OF PROFITS

The only thing Keely could not delay was a visit from the grim reaper. On November 18, 1898, Keely died, twenty-six years after his company had been founded. The company had never made a profit, never paid a dividend, and never even released a product. With Keely dead, investors were worried. Since there was no patent, no blueprints, no marketable machine, had Keely’s great discovery died with him? Was mankind to suffer because the grim reaper had come too early?

Keely’s most ardent supporter, Mrs. Bloomfield-Moore died soon after, and her son, Clarence Moore, wanted to find out whether Keely had been a scientific genius or a scam artist. Moore rented the bui

The Philadelphia Press did an expose of Keely on January 19, 1899. The newspaper reported that the sphere was carefully hidden in the cellar floor beneath Keely’s workrooms. False ceilings and floors had been ripped up to reveal mechanical belts and linkages to a silent water motor in the basement two floors below the laboratory. A system of pneumatic switches under the floor boards could be used to turn machinery on and off. This plan was provided in The New York Journal as illustrated below.lding that had housed Keely’s laboratory, hired two famous electrical engineers from the University of Pennsylvania and prowled through the building. The engineers didn’t find the “Hydro-Pneumo-Pulsating-Vacuo-Motor”, the “Compound Disintegrator” or the “Sympathetic Negative Attractor” because much of Keely’s machinery had been taken away by Keely’s supporters and investors who thought they might be able to replicate his magic. In the basement, however, they found a large cast iron hollow sphere, which had apparently been a reservoir for compressed air.

Scientists seized upon the discovery to discredit Keely and claim that the Scientific American had been correct. Perhaps Keely had pressed a control with his foot when he played the violin? Supporters of Keely thought the revelations were lies that came from an embittered son who was angry at his mother who hadn’t left her money to him. Nevertheless, his supporters maintained, if only Keely had lived a few more years, the world could have enjoyed another Industrial Revolution once Keely’s wonder machine solved mankind’s energy problems forever.

In the 115 years since Keely passed away, no other scientist has been able to replicate his discoveries. Was John Keely a Nikola Tesla whose inventions were ignored, or a Bernard Madoff who cheated foolish investors out of their money? Was Keely a scientist or a scam artist? Was Keely a professor of perfidy and postponement or the lone discoverer of the universe’s unknown secrets? You be the judge.